Learn, Discover, Invest

Explore helpful reads, market perspectives, and property insights to help buyers stay informed.

Explore helpful reads, market perspectives, and property insights to help buyers stay informed.

Choosing between furnished and unfurnished apartments is one of the first decisions buyers and renters face in the UAE property market. Each option comes with different costs, tenant expectations, and long-term implications. Furnished units appeal to convenience and short-term flexibility, while unfurnished units are often preferred for stability and personalization. This blog explains the key differences between furnished and unfurnished apartments in the UAE, along with their pros and cons for both investors and end-users. It also breaks down costs, rental potential, and practical factors to help you decide which option aligns with your goals. What Is a Furnished Apartment? A furnished apartment comes equipped with essential furniture and appliances such as beds, sofas, dining sets, white goods, and sometimes even kitchenware. These units are typically ready for immediate move-in without the need to purchase additional items. Furnished properties are commonly used for short-term rentals, corporate stays, and tenants who prefer convenience without long-term commitments. Furnished properties in Dubai are of two types: Semi-Furnished Includes basic items such as a bed, sofa, refrigerator, and stove. Suitable for tenants who want convenience with some flexibility. Fully-Furnished Includes complete furniture and appliances, allowing tenants to move in without any setup or additional purchases. What Is an Unfurnished Apartment? An unfurnished apartment is delivered without furniture, and sometimes with minimal appliances. Tenants or buyers are responsible for furnishing the space according to their preferences. These units are more common for long-term living, where tenants plan to stay for extended periods and invest in setting up their home. Key Differences This comparison highlights the key differences between furnished and unfurnished apartments to help you evaluate both options quickly. Feature Furnished Apartments Unfurnished Apartments Purpose Convenience and ready to use living Flexibility and personalisation Rental Price Higher Lower Tenant Type Short-term tenants, expats, business travellers Long-term tenants, families Lease Duration Shorter stays Longer stays Initial Setup Fully ready to move in Requires furnishing Investment Focus Higher short-term returns Stable long-term occupancy Maintenance Higher (furniture + appliances) Lower (minimal furnishings to maintain) Pros of Furnished Apartments Higher Rental Income Potential Furnished units generally command higher rents compared to unfurnished ones due to added convenience and setup. Attract Short-Term Tenants These apartments appeal to expats, business travellers, and tenants on temporary assignments. Faster Move-In Ready Tenants can occupy the unit immediately without additional setup costs. Suitable for Holiday and Short-Term Rentals Furnished properties perform well in short-term rental markets where flexibility is key. Cons of Furnished Apartments Higher Initial Investment Furnishing an apartment increases upfront costs significantly. Maintenance and Replacement Costs Furniture and appliances require upkeep and periodic replacement. Shorter Tenant Cycles Frequent tenant turnover can increase management effort and vacancy risk. Potential Wear and Tear Higher usage leads to faster depreciation of furniture and interiors. Pros of Unfurnished Apartments Lower Purchase and Setup Costs No need to invest in furniture initially, making it more budget-friendly. Long-Term Tenants Unfurnished units attract tenants who prefer stability and stay longer. Lower Maintenance Burden Fewer items to maintain reduces ongoing costs. Stable Rental Income Longer lease agreements often lead to consistent occupancy. Cons of Unfurnished Apartments Lower Rental Rates Rent is typically lower compared to furnished units. Slower Initial Occupancy (Sometimes) Tenants may take time to furnish before moving in. Less Attractive to Short-Term Renters Not suitable for tenants looking for immediate or temporary housing. Rental Yield Expectations in the UAE Rental yield depends on property type, location, and tenant demand. Furnished apartments often earn higher monthly rent due to added convenience. This can improve short-term yield in some areas. Unfurnished apartments usually have lower rent, but also lower costs. Tenants stay longer, which reduces vacancy gaps. This helps maintain steady income over time. In general, furnished units suit investors aiming for higher cash flow. Unfurnished units suit those who prefer stable returns with less turnover. Cost Comparison: Furnished vs Unfurnished Apartments Furnished apartments require a higher upfront investment due to furniture, appliances, and setup costs. These additional expenses can significantly increase the initial budget compared to unfurnished units. Unfurnished apartments, on the other hand, have lower initial costs since tenants or buyers are responsible for furnishing the space. This makes them more accessible for those with limited upfront capital. However, furnished units may generate higher rental income over time, while unfurnished units often offer lower operating costs and fewer ongoing expenses. Which Option Offers Better Returns? Furnished apartments can generate higher rental income per unit, especially in short-term rental markets. However, they also come with higher expenses and active management requirements. Unfurnished apartments may produce lower rent, but they often provide more predictable occupancy and lower operational costs. For many investors, this balance results in steady long-term performance. Factors to Consider Before Choosing Your Investment Goal: Short-term income favours furnished units, while long-term stability favours unfurnished ones. Target Tenant Type: Corporate tenants and tourists prefer furnished units, while families and long-term residents prefer unfurnished homes. Budget and Cash Flow: Furnished units require higher upfront investment and ongoing maintenance costs. Time and Management Capacity: Furnished rentals may require more involvement in terms of upkeep and tenant turnover. Which Option Should You Choose? Choose furnished apartments if your priority is higher rental income, flexibility, and short-term leasing opportunities. Choose unfurnished apartments if you prefer lower upfront costs, long-term tenants, and stable occupancy with less maintenance involvement. Your final choice should depend on your budget, investment horizon, and how actively you want to manage the property. Conclusion Furnished and unfurnished apartments in the UAE serve different purposes and attract different types of tenants. Furnished units are better suited for flexibility and higher short-term income, while unfurnished units provide stability and long-term rental consistency. The right choice depends on your financial capacity, investment strategy, and target tenant profile. Understanding these differences helps you make a more informed decision and avoid mismatched expectations when entering the UAE property market. At PropertySeller, we help buyers explore both furnished and unfurnished properties across the UAE and identify options that align with their investment or living goals. FAQ’s 1. Do furnished apartments give higher rental income? Yes. Furnished units usually command higher rent due to convenience and ready setup. They also attract tenants willing to pay more for flexibility. 2. Are unfurnished apartments cheaper to buy in the UAE? Yes. Unfurnished units have lower upfront cost since you do not pay for furniture. This makes them more affordable at the entry stage. 3. Which is better in the UAE: furnished or unfurnished apartments? There is no single better option. Furnished apartments suit short stays and higher rent goals. Unfurnished apartments suit long-term living and stable income. 4. Which option is better for investors in Dubai? Furnished units suit investors focused on higher short-term income. Unfurnished units suit those who want steady occupancy and lower management effort. 5. Do furnished apartments require more maintenance? Yes. Furniture and appliances need regular care and replacement over time. This increases upkeep compared to unfurnished units.

May 29, 2026

Read More

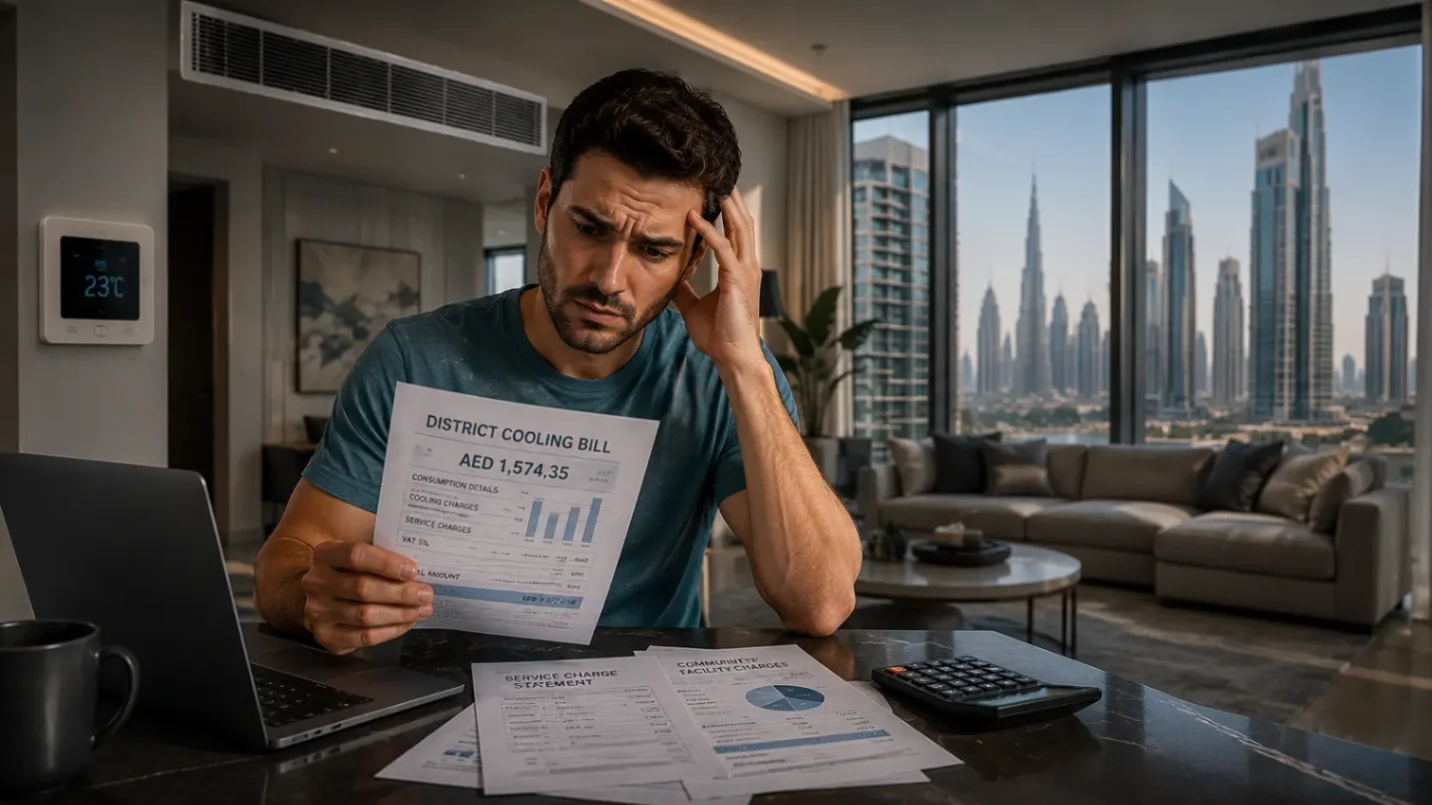

Living in the UAE means one thing for sure: air-conditioning is not optional. It runs for most of the year and directly affects your monthly expenses. In many buildings, cooling is not handled by individual AC systems. Instead, it comes through a shared network known as district cooling. District cooling is common in many communities across Dubai and other emirates. It replaces traditional air conditioning systems with a centralized cooling system. This setup affects how much you pay each month. This blog explains how it works, how costs are calculated, and what you should check before buying a property in Dubai. What Is District Cooling? District cooling is a centralized system that provides chilled water to multiple buildings from a single plant. This chilled water is used to cool indoor spaces through air-handling units. Instead of each apartment running its own cooling system, the building connects to a shared infrastructure. The cooling is distributed through underground pipes. You don’t see the system inside your home, but you pay for it through regular bills. This setup is common in large communities, high-rise towers, and master-planned developments across Dubai and other parts of the UAE. How District Cooling Works The process is simple to understand at a high level: A central plant produces chilled water using large cooling machines. This water is sent through insulated pipes to connected buildings. Inside each unit, the system uses the chilled water to cool the air before circulating it indoors. After absorbing heat, the water returns to the plant to be cooled again. The cycle continues throughout the day. This shared model allows one system to serve many buildings at once, reducing the need for separate cooling equipment in each apartment. How District Cooling Costs Are Calculated District cooling costs are not fixed in the same way as rent. They depend on multiple factors. 1. Consumption-Based Charges Some providers charge based on actual usage. Your bill increases when you use more cooling and decreases when usage drops. 2. Fixed Charges Even if usage is low, fixed fees still apply. These may include capacity charges, connection fees, or service fees. 3. Unit Size Larger apartments require more cooling, which leads to higher monthly bills. 4. Building Efficiency Older buildings or poorly insulated units may consume more cooling, increasing costs. 5. Provider Rates Different developers or cooling providers use different pricing structures. This creates variation across communities. Average District Cooling Costs in the UAE There is no single fixed price across the UAE. However, typical monthly costs can range widely depending on usage and property size. Small apartments: lower monthly charges Mid-sized units: moderate to high monthly bills Larger apartments or villas: significantly higher consumption In some cases, district cooling may form a noticeable part of your total monthly housing cost. It is also important to note that some properties include cooling charges within service fees, while others bill it separately. District Cooling Service Charges in the UAE District cooling costs in the UAE are not a simple flat fee. They include a mix of fixed and variable charges that you should know before buying. Common Charge Types 1. Capacity (Demand) Charge This is a fixed yearly cost based on your unit’s cooling capacity (measured in refrigeration tons). It is often billed monthly. For example, a system might charge around AED 750 per ton per year. 2. Consumption Charge This is based on how much cooling you actually use. Many providers bill around AED 0.62 per ton-hour consumed, measured by a meter in your unit. 3. Security Deposit Most cooling providers require a refundable deposit. This can vary by unit size — for example: Studio: ~AED 1,000 1-Bedroom: ~AED 1,500 2-Bedroom: ~AED 2,000 3-Bedroom: ~AED 3,000 4. Connection Fees There are usually two types of connection fees: A larger fee paid once by the first owner or developer (e.g., ~AED 1,500 per ton). A smaller customer/tenant connection charge (e.g., ~AED 250). 5. Meter and Maintenance Fees Monthly meter charges (~AED 25 per month) and small maintenance fees may also apply. Pros of District Cooling Centralized system: One system serves multiple buildings, reducing the need for individual units. No indoor AC equipment clutter: Apartments often have fewer visible cooling components inside the unit. Consistent performance: Cooling is generally stable across the building when the system runs properly. Reduced maintenance inside units: You don’t deal with compressors or large AC installations within your apartment. Cons of District Cooling Additional monthly expense: Cooling adds a separate cost beyond rent and service charges in many cases. Fixed fees apply regardless of use: Even with low usage, certain charges remain constant. Less control over pricing: Rates are set by the provider and not controlled by the resident. Possible billing confusion: Charges can be complex, especially for first-time buyers who are unfamiliar with the system. Dependency on the central plant: If the system faces issues, multiple buildings can be affected at once. What Buyers Must Check Before Purchasing This is where many buyers make mistakes. Skipping these checks leads to unexpected costs later. Confirm if the Property Uses District Cooling Not all buildings in the UAE use it. Some rely on individual systems. Always verify this before purchase. Ask for Sample Bills Request recent cooling bills from the seller or agent. This gives a realistic view of monthly expenses. Understand the Billing Method Find out if charges are based on usage, flat rate, or unit size. Each model impacts your cost differently. Check Connection and Transfer Fees New owners may need to pay fees to activate or transfer the cooling account. These costs can add up. Review Developer or Provider Terms Different communities follow different pricing rules. Understanding the provider helps avoid surprises. Impact on Investment Decisions District cooling affects both end users and investors. For end users, it adds to the total monthly cost of living. For investors, it influences tenant demand and rental pricing. Properties with high cooling charges may require lower rent adjustments to stay competitive. On the other hand, buildings with efficient systems may attract tenants more easily. Ignoring cooling costs during valuation can lead to unrealistic return expectations. Conclusion District cooling is a major part of many properties in the UAE. It shapes monthly expenses and affects both comfort and cost. Understanding how the system works, how bills are calculated, and what fees apply helps you avoid surprises after purchase. At PropertySeller, we help buyers evaluate properties with full cost clarity, so decisions are based on real numbers—not assumptions. We review key charges, compare options across communities, and highlight the hidden costs that often get overlooked. This helps you avoid surprises and choose a property that fits both your budget and long-term plans. FAQ’s 1. Do all properties in the UAE use district cooling? No. It is mainly used in large communities, high-rise towers, and master-planned developments. Other properties use individual AC systems. 2. Is district cooling cheaper than regular air conditioning? Not always. It depends on usage, unit size, and provider rates. Some users pay more due to fixed charges, while others benefit from efficiency in large buildings. 3. How are district cooling bills calculated? Bills usually include two parts: a fixed capacity charge and a variable consumption charge. Some providers also add meter fees and service-related costs. 4. Are district cooling charges included in rent? In some cases, yes. In many properties, cooling is billed separately. Buyers should always confirm how it is handled before signing a contract. 5. Is district cooling mandatory in certain buildings? Yes. If a building is connected to a district cooling system, residents must use it. There is no option to switch to a different cooling provider. 6. Do I need to pay a deposit for district cooling? Yes. Most providers require a refundable security deposit when setting up the account. The amount depends on the unit size.

May 29, 2026

Read More

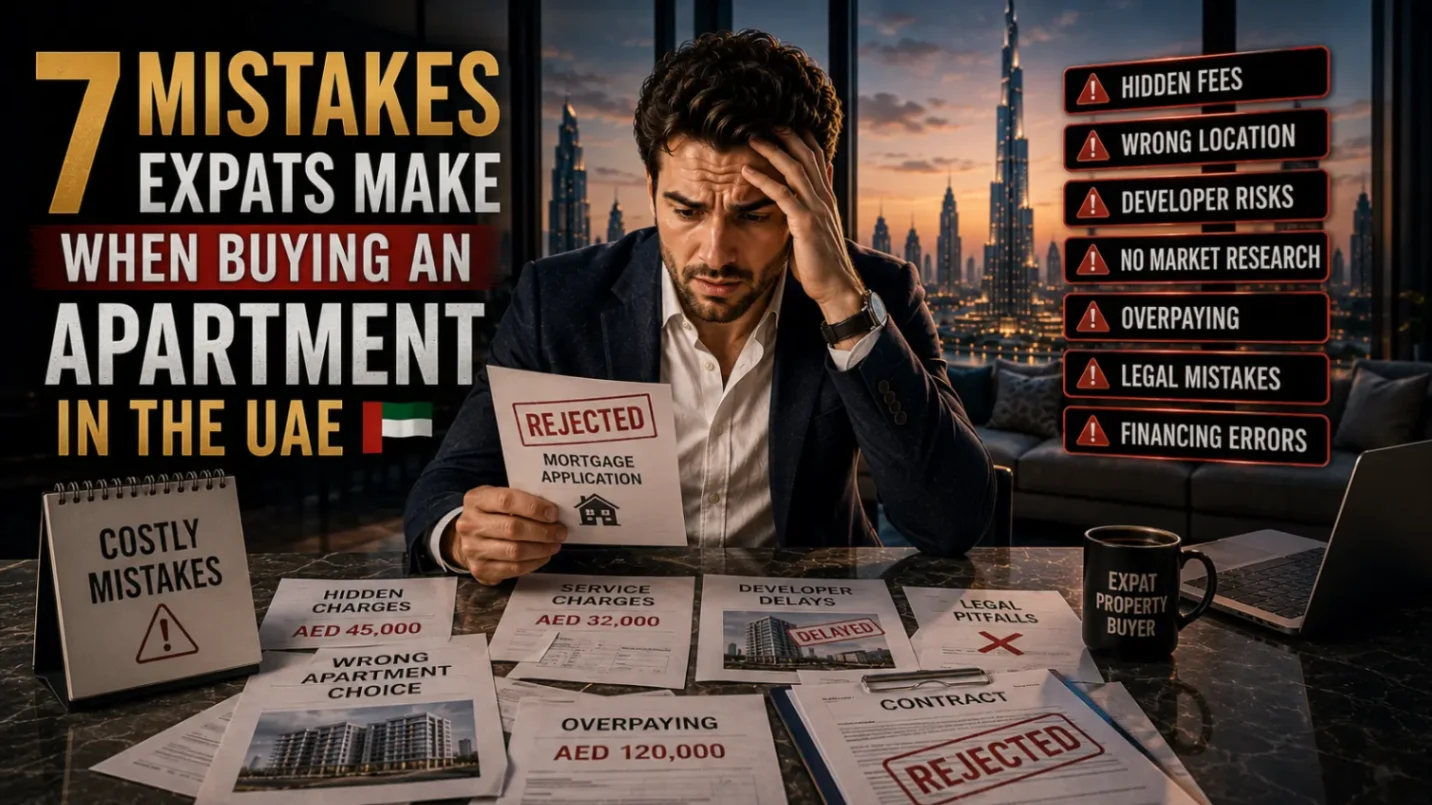

Off-plan property in Dubai attracts buyers with low entry prices and easy payment plans. It looks like a simple way to enter the market and make profit. Many investors expect prices to rise before the project is complete, giving them a quick exit. But this expectation does not always match reality. Many buyers enter the market expecting quick resale opportunities or rental income. In reality, timelines, market shifts, and project execution can change those expectations. This blog breaks down the biggest risks of off-plan property in Dubai, how they affect your money, and what you should consider before buying. What Is Off-Plan Property in Dubai? Off-plan property refers to units that are sold before construction is completed. These properties are often sold at earlier stages of development, which means buyers rely on plans, layouts, and developer commitments rather than a finished unit. Buyers purchase these properties directly from developers based on project plans and designs. Payments are usually made in stages during construction. Once the project is completed, buyers receive ownership and can either sell or rent the property. Biggest Risks of Off-Plan Property in Dubai Project Delays One of the most common risks in off-plan property is project delay. Construction timelines may extend due to approval delays, labour issues, and funding problems. When delays happen buyers may have to wait longer for handover, investment returns might be delayed, and personal plans may be affected. In some cases, delays can also affect payment schedules and increase holding costs for buyers. Market Price Changes Property prices in Dubai do not always move upward. Market conditions can change during construction. If prices drop before completion: The property may be worth less than the purchase price Selling becomes more difficult Buyers may need to hold the property longer This can affect your ability to sell at a profit or even match your initial purchase price. Developer Reliability The success of an off-plan investment depends heavily on the developer. Some developers deliver projects on time with good quality. Others may delay or reduce build quality. Buyers should always review: Past projects Delivery timelines Reputation in the market Choosing a developer without proper research increases the chance of delays or lower build quality. Limited Resale Options Selling an off-plan property before completion is not always easy. In most cases: Buyers must pay a certain percentage before resale Developer approval is required Market demand affects resale opportunities This means buyers cannot always exit their investment quickly if market conditions change. No Rental Income During Construction Off-plan properties do not generate rental income until completion. This means no cash flow during construction and longer wait to recover investment. Buyers relying on rental income should consider this carefully. Hidden Costs Apart from the property price, buyers must pay additional costs such as: Dubai Land Department fees Registration charges Service charges after handover These additional costs can reduce overall profit margins if not planned in advance. High Supply in Certain Areas Dubai often sees multiple projects launched in the same area. If many units are completed at the same time competition increases, rental prices may drop, and property value growth may become slow. When supply increases faster than demand, it can put pressure on both rental prices and property values. Property Quality Differences Buyers purchase off-plan property based on plans and marketing materials. However, the final property may differ in: Finishing quality Layout details Overall build Buyers should be prepared for minor differences. Payment Plan Risk Flexible payment plans make off-plan property attractive. However, buyers must maintain regular payments during construction. If financial situations change payments may become difficult, and penalties may apply. Missing payments can also affect the buyer’s contract and investment progress. Opportunity Cost (Important but Often Ignored) While investing in off-plan property, funds remain locked for several years. During this time: Buyers cannot use the same funds for other investments No income is generated Market opportunities may be missed This is one of the most overlooked risks, as it directly affects how efficiently your capital is used over time. Legal and Regulatory Protection Off-plan property purchases in Dubai are regulated by local authorities to protect buyers. One of the key protections is the use of escrow accounts. Payments made by buyers are held in these accounts and released to the developer in stages based on construction progress. Buyers should also ensure: The project is registered with the relevant land department Payments are made through approved channels Contracts clearly outline terms, timelines, and penalties These measures help reduce risk, but they do not remove it completely. Buyers should still verify all documents and understand the terms before making payments. How Buyers Can Reduce Risk Buyers can reduce risk by taking a few careful steps: Choose developers with strong track records Compare off-plan options with ready properties Plan finances beyond initial payments Avoid areas with too many similar projects Have a clear long-term plan before investing Doing proper research before committing helps reduce unexpected issues during the investment process. Who Should Avoid Off-Plan Property Off-plan property is not suitable for every buyer. You should reconsider if: You need quick returns Your budget is tight You rely on rental income soon You may need access to your money Off-plan works better for buyers who can wait and manage long-term risk. If your situation does not allow long waiting periods or financial flexibility, ready properties may be a better option. Conclusion Off-plan property in Dubai offers good opportunities, but it also comes with risks that buyers should understand before making a decision. From project delays to market changes, each factor affects your final return. Buyers who plan carefully and choose the right property are more likely to achieve better results. At PropertySeller, we help buyers explore verified off-plan and ready properties across Dubai. Our platform keeps the process simple and helps investors make informed decisions with confidence. FAQ’s 1. Is off-plan property safe in Dubai? Off-plan property in Dubai is regulated, and escrow accounts help protect buyer payments. However, risks still exist, so buyers should choose trusted developers and review all details before investing. 2. Can foreigners buy off-plan property in Dubai? Yes. Foreigners can buy off-plan property in designated freehold areas without needing UAE residency. 3. Can I sell off-plan property before completion? Yes, but resale depends on developer rules, payment completion percentage, and market demand. Some approvals may be required. 4. What are escrow accounts in off-plan property? Escrow accounts hold buyer payments and release funds to developers in stages based on construction progress, adding a layer of financial protection. 5. What are the main costs involved in buying off-plan property? In addition to the property price, buyers may pay registration fees, Dubai Land Department fees, and service charges after handover.

May 29, 2026

Read More

Dubai continues to attract residents, professionals, and international workers. This steady inflow creates constant demand for rental homes across the city. Areas with strong demand tend to perform better for investors who focus on rental income. This blog explains the best areas in Dubai for rental income, the type of tenants each area attracts, and the factors that affect returns. It also covers how to choose the right location based on your budget and goals. What Makes a Good Rental Area in Dubai? A good rental area is not just about low price or high rent. It depends on demand, access, and tenant profile. Key factors include: Strong tenant demand throughout the year Easy access to business hubs and transport Nearby schools, retail, and daily services Balanced property prices compared to rental value Areas that meet these conditions usually offer better occupancy and stable rental income. Rental Yield by Area Rental yield is the return earned from a property compared to its price. In Dubai, yields vary depending on location and demand. Affordable areas like International City and JVC often offer 6% to 8% yields Mid-range areas like Dubai Silicon Oasis offer 5% to 7% yields Prime areas like Downtown Dubai and Dubai Marina offer 4% to 6% yields Higher yields often come with lower property prices, while premium areas offer stability and long-term value. High-Yield vs Premium Rental Areas in Dubai Not all rental areas in Dubai perform the same. Some offer higher rental returns, while others provide stable demand and long-term value. High-yield areas focus on maximum return. These usually have lower property prices and strong tenant demand. Premium areas focus on location, lifestyle, and tenant quality. These areas offer lower yields but better stability. Choosing the right area depends on your goal. If you want higher returns, focus on yield. If you want stability and long-term growth, consider premium locations. Best High-Yield Areas in Dubai International City Average Rental Yield: 7% to 9% International City is one of the most affordable areas in Dubai, which keeps demand high among workers and small families. The area offers basic living with easy access to main roads and daily services. Because of low property prices and steady tenant demand, occupancy rates remain strong throughout the year. This makes it a practical choice for investors focused on higher rental returns. Jumeirah Village Circle (JVC) Average Rental Yield: 6% to 8% JVC is a growing residential community that attracts families and mid-income professionals. It offers a quieter lifestyle with parks, schools, and improving retail options. The combination of affordable pricing and rising demand makes it a strong choice for consistent rental income and long-term occupancy. Dubai Sports City Average Rental Yield: 7% to 9% Dubai Sports City is known for its lower property prices and steady demand from young professionals and budget tenants. The area offers open spaces and a relaxed environment focused on sports and fitness. Smaller units perform well here, making it suitable for investors targeting higher yields with lower entry costs. Dubai Silicon Oasis Average Rental Yield: 5% to 7% Dubai Silicon Oasis attracts tech professionals and families looking for affordable housing. It is a planned community with schools, offices, and daily facilities within reach. Stable tenant demand and reasonable pricing support long-term rental income with lower vacancy risk. Premium Areas With Strong Rental Demand Dubai Marina Average Rental Yield: 5% to 6% Dubai Marina is a popular waterfront area known for its lifestyle, dining, and walkable spaces. It attracts young professionals and expats who prefer living close to key locations. Strong demand and limited waterfront supply help maintain stable rental income throughout the year. Downtown Dubai Average Rental Yield: 4% to 5% Downtown Dubai is a premium location with luxury apartments and high-end living. It attracts business professionals and short-term renters due to its central location. While yields are lower, tenant quality is strong and property values remain stable over time. Business Bay Average Rental Yield: 5% to 6% Business Bay is a central district close to major business hubs and offices. It attracts working professionals who want to reduce commute time. The mix of residential and commercial spaces supports steady rental demand and consistent occupancy. Average Property Prices by Area Property prices in Dubai vary based on location, building quality, and unit type. Below is a general overview of starting apartment prices in the key rental areas: AREA Starting Price Dubai Marina AED 1.1M - 1.4M Jumeirah Village Circle AED 600K - 700K Downtown Dubai AED 1.1M - 1.3M Business Bay AED 900K - 1.1M Dubai Silicon Oasis AED 650K -1.3M International City AED 450K - 900K Dubai Sports City AED 550K -1.6M These prices are approximate and may vary based on unit size, building, and market conditions. Buyers should always compare current listings before making a decision. Explore apartments for sale in Dubai and start your investment with the right opportunity. Why Invest in Dubai Real Estate Dubai offers strong rental demand, no annual property tax on income, and a growing population of residents and expats. This creates steady demand for rental homes across key areas. The market is also regulated, with systems like escrow accounts that help protect buyers. Combined with modern infrastructure and global appeal, Dubai remains a reliable option for both rental income and long-term value. How Buyers Can Choose the Right Area Choosing the right area depends on your investment goal. For higher yields, focus on affordable areas For stable tenants, choose central locations For long-term value, consider premium areas Buyers should also compare service charges, tenant demand, and total cost before making a decision. Conclusion Dubai offers a range of areas suitable for rental income, each with different advantages. Some areas provide higher yields, while others offer stability and long-term growth. The right choice depends on your budget, expected returns, and risk level. At PropertySeller, we help buyers explore verified properties across Dubai and identify areas that match their rental income goals. Our platform simplifies the process and supports better investment decisions. FAQ’s 1. Is Dubai a good place for rental property investment? Yes. Dubai has strong demand from residents and expats, no annual property tax, and a growing rental market. 2. Which type of property is best for rental income? Studios and one-bedroom apartments often perform well due to higher demand and lower entry costs. 3. What is the average rental yield in Dubai? Rental yields in Dubai typically range between 5% to 8%, depending on the area, property type, and market conditions. 4. Which area in Dubai gives the highest rental income? Areas like Dubai Marina, Downtown Dubai, and Business Bay often generate strong rental income due to high demand and prime locations. 5. Can foreigners invest in rental property in Dubai? Yes. Foreign investors can buy property in designated freehold areas across Dubai, including locations that support rental income.

May 29, 2026

Read More

Buying an apartment in the UAE looks straightforward. But many buyers overlook one factor that quietly affects everything—maintenance fees. Two apartments in the same area can have completely different service charges. One performs well. The other drains your returns. Most investors don’t understand why this happens until it’s too late. This is not just about cost. It is about how your investment behaves over time. If you don’t understand maintenance fees properly, your numbers will never be accurate. This blog explains what drives high maintenance fees in UAE apartments, how they are calculated, and why they vary so much between buildings, along with how they influence rental performance and long-term value. What Most Property Websites Get Wrong Most platforms explain maintenance fees at a surface level. They tell you what is included—cleaning, security, maintenance—and give a general cost range. That is basic information. It does not help you make a decision. What they fail to explain is: Why newer buildings sometimes have higher fees than older ones Why poorly managed buildings become more expensive over time Why high fees reduce buyer interest when you try to sell This is where most investors miscalculate. They see numbers but don’t understand the behaviour behind those numbers. The Real Reasons Some Apartments Have High Maintenance Fees Maintenance fees are not random. They are driven by specific factors. If you don’t break these down, you are just guessing. 1. Facilities and Amenities The more a building offers, the more it costs to maintain. Buildings with multiple pools, large gyms, concierge services, and smart systems will always have higher service charges. What most buyers ignore is utilization. You may not use all the facilities, but you still pay for their upkeep, staffing, and operation. 2. Building Design and Complexity This is one of the most ignored factors. High-rise towers with multiple elevators, centralized cooling systems, and complex layouts require more maintenance. Glass-heavy buildings, for example, require frequent cleaning. That alone increases ongoing costs. 3. Developer Quality Not all developers build with the same standards. Some prioritize long-term durability, while others focus on rapid delivery and sales. Poor construction quality leads to: Frequent repairs Higher maintenance cycles Increasing service charges over time This is not visible at the time of purchase. But it shows up later in your expenses. 4. Community Management Efficiency This is where things get serious. A well-managed building controls costs. A poorly managed one inflates them. Bad management leads to: Overpriced vendor contracts Unnecessary repairs Lack of cost control Two similar buildings can have very different fees purely based on how they are managed. 5. Occupancy Levels Low occupancy increases your cost per unit. If fewer owners are paying into the system, the cost gets distributed among a smaller group. That pushes fees higher. This is common in newly launched projects or investor-heavy communities with a high number of vacant units. 6. Location Positioning Prime areas like Downtown Dubai or Dubai Marina often have higher service charges. Why? Because expectations are higher: Better upkeep Premium services High-end presentation You are not just paying for maintenance. You are paying for positioning. How High Maintenance Fees Affect Your Returns Most investors calculate returns like this: Rental income – purchase price = yield That is incomplete. You need to subtract: Service charges Maintenance costs Vacancy periods A property with high rent but high maintenance fees can underperform compared to a lower-rent unit with minimal expenses. Ignoring these costs leads to inflated expectations and inaccurate projections. What Our Data Actually Shows (Beyond Listings) Most platforms show listings. They don’t show behaviour. At PropertySeller, our internal data tracks: Actual rental consistency Vacancy trends across buildings Buyer response to high-fee properties Here’s what the data shows clearly: High-fee apartments attract tenants slower Tenant turnover is higher in overpriced buildings Buyers negotiate harder on high service charge units This is the difference between advertised value and real performance. How to Identify Risk Before You Buy If you’re serious about investing, you need to stop thinking like a buyer and start thinking like an operator. Before you buy, check: Cost per sq ft, not just total fee Building age and repair history Occupancy levels Developer reputation Management quality If you skip this, you are not investing—you are hoping. Why Cheaper Service Charges Are Not Always Better Lower maintenance fees are not automatically beneficial. In some cases, they indicate deeper issues. Possible downsides include: Reduced maintenance quality Deteriorating building condition Lower tenant attractiveness This can result in: Lower achievable rents Difficult resale Faster depreciation of the property The objective is not minimizing cost, but ensuring cost efficiency aligned with property quality. Our View as Property Sellers We consistently observe the same pattern among buyers. Many focus heavily on purchase price while ignoring long-term operating costs. Apartments with high maintenance fees are not inherently bad, but they must justify their costs through: Strong tenant demand Stable rental performance Sustained long-term value At PropertySeller, we go beyond listings. We analyse how properties perform over time using verified data on tenant movement, vacancy trends, and transaction behaviour—not just advertised figures. To explore options, you can review luxury apartments for sale in Dubai. Final Thoughts High maintenance fees are a key factor in determining the real performance of a property. They directly influence rental income, buyer interest, and resale outcomes. Apartments with higher charges are not necessarily poor investments, but they require stronger justification in terms of location, demand, and management efficiency. Without understanding the reason behind the cost, investors risk overpaying and underestimating ongoing expenses. At PropertySeller, we prioritize clarity and accuracy. Your data remains protected, and every listing is verified to ensure reliability. This allows you to evaluate opportunities with confidence and make informed investment decisions instead of relying on incomplete information. FAQs 1. Why do some UAE apartments have higher maintenance fees? Because of factors like facilities, building design, management quality, and location positioning. 2. Do high maintenance fees mean better quality? Not always. Some buildings charge more without delivering better value. 3. How do maintenance fees affect rental yield? They reduce your net income, which lowers your actual return. 4. Are high service charge properties harder to sell? Yes. Buyers compare ongoing costs, which affects demand and pricing. 5. How can I check if maintenance fees are reasonable? Compare cost per sq ft, building condition, and rental performance—not just total charges.

May 29, 2026

Read More

Buying a property in Dubai may seem simple on the surface, but the outcome depends on how well you understand each step involved. Most people treat it as a checklist, but the process is actually decision-driven. Each step you take influences the next, and a mistake early on can restrict your options later. This guide breaks down the actual process used in Dubai, but more importantly, highlights what matters at each stage so you can make informed decisions rather than just follow steps. Step 1: Define Your Investment Goal Before looking at properties, you need clarity on why you are buying. Are you buying for rental income, capital appreciation or personal use. This decision determines location, property type, budget structure, and financing approach. Skipping this step leads to inconsistent choices and poor returns. Step 2: Understand Your Budget and Financing Options Your budget is not just the property price. It includes: Down payment Transfer fees Agency commission Mortgage costs (if applicable) Maintenance and service charges For expats, mortgage eligibility depends on: Income stability Credit history Debt-to-income ratio Employment profile Banks evaluate risk, not just affordability. Getting pre-approved helps you understand your real purchasing power before committing. It also gives you clarity on loan limits, interest expectations, and avoids delays during the purchase process. Step 3: Choose Between Ready and Off-Plan Property Once your budget and goal are clear, the next step is deciding the type of property. In Dubai, you can buy either ready or off-plan properties. Ready Properties Off-plan Properties Immediate ownership Lower initial entry cost Rental income potential Flexible payment plans Lower uncertainty Longer completion timeline Ready properties provide immediate usability and income potential. Off-plan can look attractive, but it introduces risks like construction delays and market changes. Your choice should align with your timeline and risk tolerance. Explore off plan apartments for sale in Dubai for more… Step 4: Shortlist Properties Based on Demand, Not Just Price Focusing only on price per square foot is a common mistake. A more effective approach is evaluating long-term demand indicators such as: Tenant demand in the area Vacancy rates Future supply pipeline Infrastructure development Areas with high demand tend to perform better over time. Price alone does not determine value. Step 5: Verify the Property and Legal Status Before proceeding, ensure the property is legally secure and properly documented: Confirm registration and approval Check developer credibility Verify there are no disputes or liabilities For ready properties, review title deed. For off-plan, confirm project registration and developer authorization. This step protects you from legal and financial risks. Step 6: Make an Offer and Sign the Agreement Once you finalize a property: Submit an offer through the agent Negotiate and agree on terms Sign a Memorandum of Understanding (MoU) At this stage, you typically pay a deposit (commonly around 10%). The MoU outlines price, payment terms, timelines, and obligations of both parties. It is a legally binding agreement. Step 7: Arrange Mortgage (If Applicable) If you are financing the purchase: Apply for mortgage approval Submit required documents (income proof, bank statements, etc.) Undergo property valuation Banks will assess both your profile and the property value before final approval. Delays or rejections often occur if valuation or eligibility criteria are not met. Step 8: Complete Transfer at the Dubai Land Department The final transfer is handled through the Dubai Land Department and a registered trustee office. At this stage: Remaining payment is settled Ownership is transferred Title deed is issued Once completed, the property is officially yours. Step 9: Register and Take Possession After transfer: Register utilities (DEWA, etc.) Arrange property management (if needed) Take possession of the property If the property is intended for investment, it can now be rented out or managed through a property management service. How Long Does it Take to Buy a Property in Dubai? The timeline depends on the type of property, financing method, and preparedness of the buyer. For ready properties, the process can be completed relatively quickly. Once an offer is accepted and the Memorandum of Understanding (MoU) is signed, the transfer at the Dubai Land Department can typically be completed within a few days, provided mortgage approval (if applicable) is already in place. For off-plan properties, the timeline follows the developer’s payment plan and construction schedule. In such cases, the purchase is completed over months or years, depending on project milestones. If financing is involved, mortgage pre-approval may take a few days, while final approval depends on document verification and property valuation. Buyers who prepare documentation in advance experience fewer delays. In most cases, a ready property purchase with pre-approved financing can be completed within 1 to 3 weeks, while off-plan purchases follow a longer, phased timeline aligned with construction progress. The Step Most People Underestimate The biggest issue is not the purchase itself, but the order in which decisions are made. Most people choose property first, then check financing only to realize limitations that could have been avoided earlier. This can lead to compromises, renegotiations, or even failed approvals. The correct approach is: Financing → Budget clarity → Strategy → Property selection Common Mistakes Expats Make Skipping mortgage pre-approval Ignoring total upfront costs Choosing property based on emotion instead of demand Not verifying legal status Underestimating ongoing expenses These mistakes don’t show up immediately. They appear later as financial pressure or poor returns over time. Conclusion Buying property in Dubai is not just a transaction—it’s a structured process that requires planning, verification, and timing. Each step builds on the previous one, and skipping or rushing any part can affect your outcome. At PropertySeller, we focus on verified listings and data-backed insights so buyers can move through this process with clarity. Every property is evaluated beyond price, helping you understand true value, financing impact, and long-term potential before making a decision. FAQ’s 1. Can expats buy property in Dubai? Yes, expats can buy property in designated freehold areas in Dubai with full ownership rights. 2. Do I need a visa to buy property in Dubai? No visa is required to purchase property, but certain investments may make you eligible for a residency visa depending on the property value and regulations. 3. What is the minimum budget to buy property in Dubai? It depends on the location and property type. Entry-level properties can start from lower price ranges, but buyers should also account for down payment, fees, and additional costs beyond the listing price. 4. How much down payment is required for a mortgage? For expats, banks typically require a down payment ranging from 20% to 25% of the property value, depending on the property price and your financial profile. 5. Are there any hidden costs when buying property in Dubai? Yes. Buyers should consider transfer fees, agency commissions, mortgage fees, registration fees, and ongoing maintenance or service charges. 6. How long does property transfer take in Dubai? If financing is ready and documents are in order, the transfer through the Dubai Land Department can often be completed within a few days for ready properties.

May 29, 2026

Read More

Buying property in the UAE is no longer just about rental income or long-term appreciation. For many investors, it has become a direct pathway to residency. This is where the UAE Golden Visa stands out. But most buyers approach this the wrong way. They hear “buy property, get visa” and assume the process is automatic. It is not. The eligibility rules, payment structure, and legal conditions matter more than the property itself. This guide explains how the Golden Visa works through real estate investment. It covers requirements, fees, process, and the key factors that determine whether you qualify. More importantly, it highlights the practical gaps most investors miss when they focus only on eligibility and ignore investment quality.. What Is the UAE Golden Visa? The UAE Golden Visa is a long-term residency program designed to attract investors, entrepreneurs, and professionals. For property investors, it offers residency for 5 or 10 years, depending on the investment value. Unlike standard visas, it does not require a local sponsor or employer. Your residency is tied to your asset, not your job. This gives investors long-term stability and flexibility. You are not dependent on employment renewals, which changes how you plan both your finances and your stay in the UAE. Golden Visa Eligibility: What Actually Qualifies This is where most investors get it wrong. To qualify for a UAE Golden Visa through property investment: Total property value must be at least AED 2 million The property must be in a freehold area Ownership must be legally registered The property should be completed or meet approved payment thresholds You can qualify using a single property or multiple properties combined. But here’s the detail most people ignore. If the property is financed, eligibility depends on how much has been paid, not just the total value. This means a AED 2M property does not automatically qualify you if a large portion is still financed. This is where buyers get misled. They assume price equals eligibility, when in reality, payment structure matters just as much. Golden Visa Fees for Property Investors Beyond the investment itself, there are administrative costs involved in securing the visa. These typically include: Visa application charges Medical fitness test Emirates ID issuance Health insurance Government processing fees In total, investors should expect around AED 3,000 to AED 6,000+, depending on visa duration and application channel. These are not major costs compared to property value, but ignoring them leads to incomplete financial planning. Key Benefits of UAE Residency by Investment The Golden Visa offers more than long-term residency. It changes how investors operate within the UAE. Key advantages include: Long-term residency (5 or 10 years) No need for a local sponsor Ability to sponsor family members Flexibility to stay outside the UAE without visa cancellation Access to banking, business, and financial systems But the real advantage is independence. Your residency is not tied to employment or short-term renewals. That stability allows you to plan long-term, both personally and financially. How to Apply for a Golden Visa Through Property The process is straightforward if your property meets eligibility conditions. It generally follows these steps: Purchase a qualifying property Obtain the title deed from the Dubai Land Department Submit the Golden Visa application Complete medical and biometric checks Receive Emirates ID and residency visa Most investors use professional services to avoid delays caused by documentation errors or eligibility confusion. Freehold vs Leasehold: Why Ownership Type Matters Golden Visa eligibility is directly linked to ownership. Only properties in designated freehold areas qualify. Leasehold properties typically do not meet the criteria because they do not provide full ownership rights. This limits your options. Buyers who ignore this often end up with a property that cannot support their residency goal. This is not just a legal detail—it directly affects your investment flexibility. Off-Plan vs Ready Property: The Timing Gap Many investors assume off-plan properties automatically qualify for a Golden Visa. That is not always true. Eligibility depends on: Payment completion level Developer approval Project status In most cases, a property must be completed or significantly paid for before it qualifies. This creates a gap. You may invest today but only become eligible later. If you don’t plan for this, your expectations and cash flow won’t align. The Investment Reality Most Buyers Ignore Here is the part most websites avoid explaining clearly. When investors target the Golden Visa, they often prioritize hitting the AED 2 million threshold. This shifts focus away from investment performance. Higher-value properties: Often deliver lower rental yield Require larger capital commitment Take longer to resell So the decision becomes strategic. Are you investing for UAE residency, or for returns? If the goal is not clearly defined, the outcome is usually average on both sides. A property chosen only for visa eligibility may not perform well financially. Can Multiple Properties Be Combined? Yes, Investors can combine multiple properties to meet the AED 2 million requirement. However: All properties must be under the same ownership Combined value must reach AED 2 million Documentation must clearly support the valuation This approach works for investors who already own smaller units and want to qualify without entering a higher price segment. What Happens If You Sell the Property? Golden Visa eligibility is tied to your investment status. If the property is sold: Visa eligibility may be affected Renewal may not be possible Reinvestment may be required This makes exit planning important. You are not just buying an asset—you are linking it to your residency. Common Mistakes Investors Make Most issues come from assumptions rather than lack of information. Investors often: Assume any property qualifies Ignore mortgage-related eligibility rules Focus only on visa benefits, not investment quality Skip proper legal and ownership verification These mistakes are avoidable, but only if decisions are based on structure, not marketing claims. Final Thoughts The UAE Golden Visa through property investment is a strong opportunity, but only if you understand how it actually works. It is not just about buying a property above a certain value. It is about meeting specific conditions, managing costs, and aligning your investment with your goal. At PropertySeller, we approach this differently. We focus on verified properties that align with both Golden Visa eligibility and long-term investment value. Your data stays secure, and every listing is checked so you can make decisions based on clear, reliable insights— so you don’t just qualify for a visa, but invest in something that holds real value over time. FAQ’s 1. Can you get a UAE Golden Visa with a mortgage? Yes. You can get a UAE Golden Visa with a mortgaged property, but the paid amount must usually reach AED 2 million, not just the total property value. 2. What is the minimum investment for a UAE Golden Visa? The minimum property investment for a UAE Golden Visa is AED 2 million. This can be one property or multiple properties combined under your name. 3. Do off-plan properties qualify for a Golden Visa in the UAE? Off-plan properties can qualify, but only if a significant portion is paid and the project meets approval conditions. Ready properties are easier for eligibility. 4. How long does it take to get a UAE Golden Visa through property? Getting a UAE Golden Visa through property usually takes 2 to 4 weeks after submitting all required documents and approvals. 5. What happens to your Golden Visa if you sell your property? If you sell your property, your UAE Golden Visa may be cancelled unless you reinvest in another qualifying property worth AED 2 million or more.

May 29, 2026

Read More

Entering the UAE property market without understanding down payment rules is one of the fastest ways to miscalculate your investment. Most expats focus on property price and monthly installments, but the real barrier is the upfront capital requirement. On paper, it looks simple—20% or 30%. In reality, it controls your loan approval, your risk level, and whether your deal even goes through. This is where planning either works—or breaks completely. This guide explains how down payments actually work in the UAE, what banks really look at, and the critical factors most buyers ignore until it’s too late. What Is a Down Payment? A down payment is the upfront amount you pay from your own funds when purchasing a property. The remaining amount is typically financed through a mortgage if you are not buying in cash. In simple terms: Property Price = Your Down Payment + Bank Loan For expats, this upfront payment is not optional. It is a mandatory requirement set by UAE banking regulations. Why Down Payment Matters More Than You Think Most buyers treat down payment as just an entry requirement. That is shallow thinking. Your down payment directly impacts: Loan approval chances Interest rates offered by banks Monthly mortgage burden Overall investment risk A higher down payment reduces your financial pressure. A lower one increases your dependency on financing and market conditions. This is where most expats misjudge. They stretch to enter the market, instead of structuring a stable investment. Down Payment Rules for Expats UAE Central Bank regulations define how much expats must pay upfront when buying property with a mortgage. Typical requirements: 20% down payment for properties below AED 5 million 30% down payment for properties above AED 5 million Example: If you buy a property worth AED 1,000,000, minimum down payment = AED 200,000 This does not include additional costs like fees, which many buyers ignore. Additional Upfront Costs Most Expats Miss Here’s where your calculation usually falls apart. Your down payment is not your total upfront cost. You must also pay: 4% transfer fee Registration and trustee fees Agent commission (usually ~2%) Mortgage processing fees Property valuation charges Realistically, expats should plan for 25% to 30% of property value as total upfront cost. If you only prepare for 20%, you are underfunded before you even start. Mortgage Limits and Loan-to-Value (LTV) Banks in the UAE follow a system called Loan-to-Value (LTV). LTV determines how much the bank will finance. For expats: Max LTV = 80% (for properties under AED 5M) Max LTV = 70% (above AED 5M) This is directly linked to your down payment. Higher LTV = lower down payment Lower LTV = higher down payment But here’s the reality – banks don’t just follow rules—they assess risk. Your salary, job stability, credit history, and existing liabilities all affect approval. Cash Buyers vs Mortgage Buyers Not all expats use financing. Some buy in cash. Cash buyers: Avoid bank restrictions Skip mortgage-related costs Have stronger negotiation power But they still pay: Full property value upfront All transfer and registration fees So while cash removes financing pressure, it increases capital exposure. Off-Plan Properties: Different Down Payment Structure Off-plan properties follow a completely different model. Instead of a single upfront payment, developers offer payment plans. Typical structure: 10% to 20% booking amount Installments during construction Balance on completion This looks easier—but it comes with risk. Key issues: Delayed project timelines Market fluctuations during construction Limited resale flexibility before completion Many expats choose off-plan because of lower initial entry. But they don’t evaluate long-term impact. The Hidden Factor Competitors Don’t Explain Here’s what most property websites avoid. Your down payment directly affects your exit flexibility. If you enter with minimal capital: Your loan is higher Your profit margin is thinner Your ability to sell quickly is reduced But it goes deeper than that. In a slow or declining market, highly leveraged properties can fall into negative equity—where your outstanding loan is close to or even higher than the market value of the property. When that happens: Selling becomes difficult without taking a loss Buyers gain stronger negotiation power You lose flexibility to exit at the right time This is not visible when you buy. It only shows when the market shifts—and by then, your options are limited. A higher down payment does not just reduce risk. It gives you control when conditions change. That control is what most investors underestimate. How Down Payment Affects Your Investment Strategy You are not just choosing how much to pay. You are choosing your entire investment structure. Lower down payment: Higher leverage Higher risk Higher dependency on rental income Higher down payment: Lower risk Better cash flow More stability There is no “best” option. But choosing blindly is a mistake. What Our Data Shows (Beyond Listings) Most platforms show prices. They don’t show behavior. From our internal data tracking: Buyers with higher upfront investment hold properties longer Lower down payment investors face more resale pressure Mortgage-heavy buyers are more sensitive to market shifts This is not a theory. It is actual transaction behavior. Listings don’t show this. But it defines your outcome. Common Mistakes Expats Make The same patterns repeat: Planning only for 20% and ignoring extra costs Assuming loan approval is guaranteed Choosing property based on budget, not sustainability Ignoring how financing affects resale Underestimating total capital required These are not small mistakes. They change your entire investment result. How to Plan Your Down Payment Smartly If you want to approach this properly: Calculate total upfront cost, not just down payment Keep buffer funds beyond minimum requirement Compare financing vs cash scenarios Align property choice with your financial stability Think about exit before entry If you skip this, you are not planning—you are reacting. Final Thoughts Down payment is not just an entry step. It shapes your risk, your returns, and your flexibility as an investor. Most expats focus on how to enter the market. Very few think about how their entry affects long-term performance. At PropertySeller, we focus on verified data and real investment behaviour. Every property is evaluated beyond price, so you understand actual cost, financing impact, and long-term potential. This helps you invest with clarity, not assumptions. FAQ’s 1. What is the minimum down payment for expats buying property in the UAE? Expats must pay at least 20% down payment for properties below AED 5 million and 30% for properties above AED 5 million, as per UAE Central Bank regulations. 2. Can expats buy property in the UAE with a low down payment? No. UAE banks do not allow zero or very low down payments for expats. A minimum of 20% is mandatory, and buyers must also cover additional fees separately. 3. Does the down payment include Dubai property fees? No. The down payment only covers part of the property price. Buyers must separately pay fees like the 4% transfer fee, registration charges, and agent commission. 4. Can expats get a mortgage in the UAE without a down payment? No. UAE mortgage rules require expats to contribute their own funds upfront. Banks will not finance 100% of the property value. 5. How much total cash do expats need to buy property in the UAE? Expats should plan for around 25% to 30% of the property value, including down payment and all additional costs like fees and charges.

May 29, 2026

Read More

Buying an apartment in the UAE feels straightforward. You pick a property, arrange payment, and expect returns. But most expats approach this with the wrong mindset. They focus on what they can afford, not what actually works as an investment. That is where problems begin. These are structural mistakes that affect your returns, resale, and long-term value. This blog breaks down the 7 real mistakes expats make—not surface-level errors, but the ones that affect your return, resale, and long-term outcome. More importantly, it explains what most property websites don’t tell you. 1. Treating Listings as Market Reality This is the most dangerous mistake—and almost no blog talks about it properly. Listings show asking price, not actual transaction value. There is often a gap between: What sellers list What buyers actually pay If you don’t check real transaction data: You overpay Your resale margin disappears Your yield drops instantly This is where most investors lose money before they even start. 2. Choosing Based on Budget Instead of Performance Most expats start with: “What can I afford?” Wrong question. The real question is: “What performs best within my capital?” Cheap areas often come with weak rental demand, higher vacancy, and poor resale. Affordability is not a strategy. It's a limitation. 3. Ignoring Total Cost of Ownership Competitors mention “service charges,” but not the full picture. Real cost includes: Service charges Maintenance Vacancy loss Financing costs Buyers who ignore this think they’re getting 7–8% returns. In reality, they’re getting closer to 4–5%. 4. Falling for “Off-Plan Illusion” Off-plan looks attractive because: Lower upfront cost Flexible payment plans But here’s what most blogs don’t emphasize enough: Delays affect returns Market conditions change Final value may not match expectations Nearly a large share of transactions are off-plan, which increases competition and risk. If you don’t factor timing risk, your investment plan collapses. 5. Misunderstanding Demand, Not Just Location Competitors say “location matters.” That’s obvious. What they don’t explain is: Demand type matters more than location name. Example: High-demand area ≠ high demand for your unit type Studios vs family units behave differently. Short-term vs long-term tenants behave differently. If you don’t understand demand structure: You face vacancies You attract unstable tenants 6. Ignoring Exit Strategy Completely Most expats think: “I’ll deal with selling later.” That’s lazy thinking. Before buying, you should know: Who your future buyer is What they care about What will limit your resale Oversupplied buildings = slower exit High service charges = fewer buyers Exit is not optional. It’s part of the investment. 7. Trusting Platforms More Than Data Most buyers rely heavily on platforms. But here’s the truth: Platforms show listings, not reality. They don’t show: True sale prices Negotiation gaps Failed transactions That creates a false sense of market value. At PropertySeller, we focus on: Real transaction behaviour Vacancy patterns Demand consistency Because listings don’t tell you how a property performs—only how it is marketed. The Pattern Behind These Mistakes Every mistake comes from the same mindset: Short-term thinking Over-reliance on visible data Ignoring hidden variables That’s why two investors with the same budget get completely different results. How to Actually Buy Smart If you want to avoid these mistakes: Compare price per sq ft with real transactions Calculate net yield, not gross Study demand by unit type Evaluate service charge efficiency Plan your exit before entry This is not complicated. But it requires discipline most buyers don’t have. Final Thoughts Buying an apartment in the UAE is easy. Buying the right one is not. Most expats don’t fail because of the market. They fail because they trust surface-level information and make decisions without understanding how properties actually perform. At PropertySeller, we approach this differently. We go beyond listings and focus on verified data, real performance trends, and transparent insights—so you don’t just buy a property, but make a decision that holds value over time. FAQ’s 1. What is the biggest mistake expats make when buying property in the UAE? The biggest mistake is overpaying by relying on listing prices instead of real market value. Many buyers don’t compare actual transaction prices, which reduces their returns from day one. 2. How do expats avoid overpaying for apartments in the UAE? Expats can avoid overpaying by comparing price per square foot, checking recent sales data, and not relying only on property listings or agent quotes. 3. What hidden costs should expats consider when buying property in the UAE? Expats should consider service charges, maintenance, vacancy periods, and transaction fees. Ignoring these costs leads to lower real returns than expected. 4. Is buying off-plan property risky for expats in the UAE? Yes, off-plan property can be risky due to project delays, market changes, and uncertain final value. Buyers should evaluate developer reputation and project timelines before investing. 5. How important is resale value when buying property in the UAE? Resale value is critical. Properties with high service charges, poor location demand, or oversupply are harder to sell and often require price reductions.

May 29, 2026

Read More

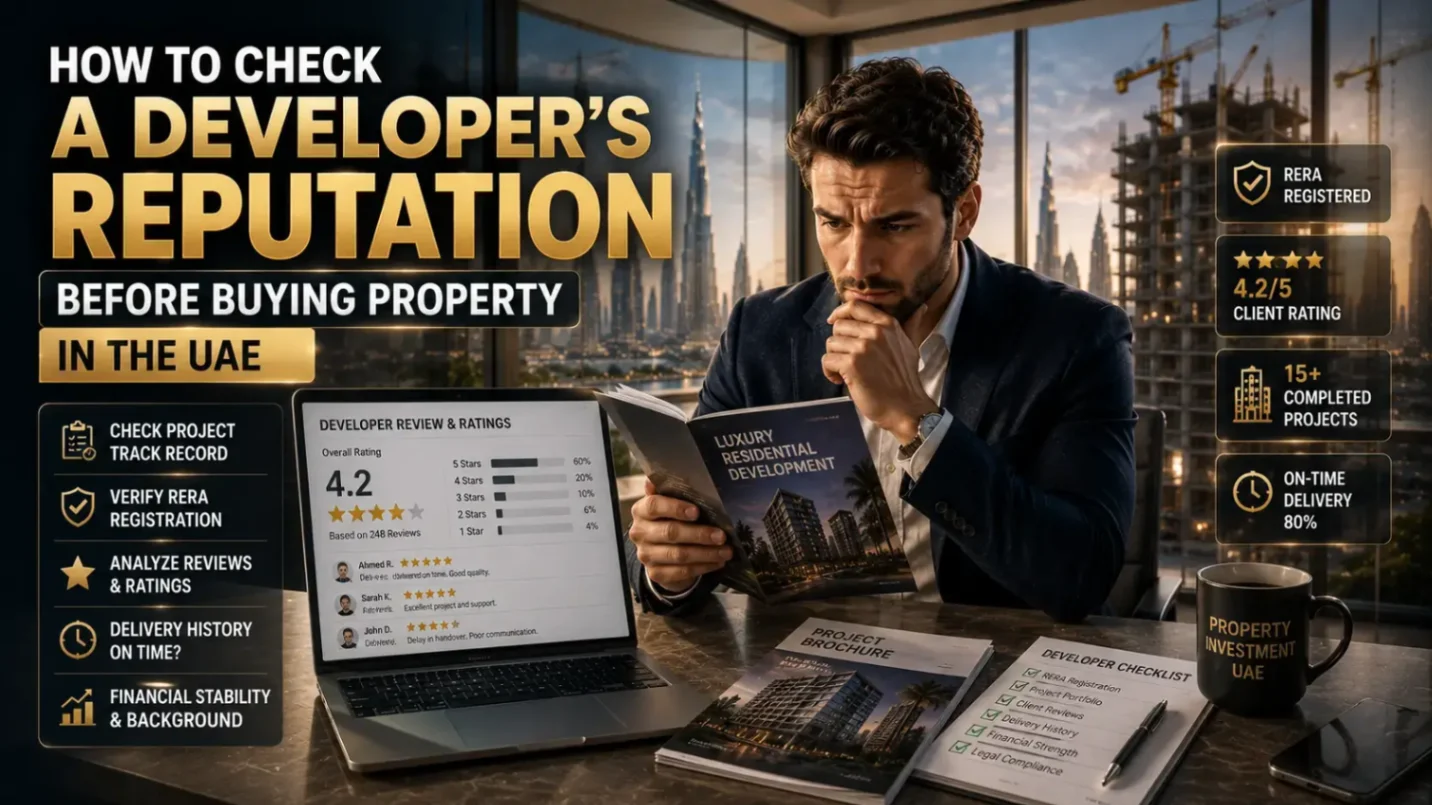

Buying property in the UAE is not just about location or price. The developer behind the project matters just as much. A strong developer can deliver quality and on time. A weak one can delay your project, cut corners, or create problems that affect your return. Many buyers ignore this step. They trust marketing, visuals, and promises. That is where mistakes happen. This blog explains how to properly check a developer before you commit your money. Why Developer Reputation Matters When you buy a property, especially off-plan, you are trusting the developer to deliver what was promised. If the developer has a poor track record, you may face: project delays quality issues changes in layout or finish resale problems This is not rare. It happens more often than most buyers expect. A good developer reduces risk. A bad one increases it, no matter how good the project looks on paper. Check Past Projects, Not Promises The first step is simple. Look at what the developer has already built. Visit completed projects if possible. Check build quality, maintenance, and how the building looks after a few years. A developer’s real reputation is not in ads. It is in their finished work. Look for build quality, condition after handover and how well the project is maintained. If older projects look poorly managed, expect similar results in new ones. Delivery History Tells You Everything One of the biggest risks in the UAE market is delay. Many developers promise timelines they cannot meet. Buyers then wait months or even years beyond the expected handover date. Check if the developer has delivered projects on time in the past. If delays are common, you should treat that as a warning, not an exception. Check Registration and Approval Every developer in Dubai must be registered with the Dubai Land Department (DLD). You can also verify projects through the Real Estate Regulatory Agency (RERA) to confirm if they are approved. If a project is not properly registered, you are taking unnecessary risk. This step is basic. Skipping it is careless. Look at Escrow Account Compliance In the UAE, off-plan projects must use escrow accounts. This means buyer payments are linked to construction progress. This protects your money. Check if the developer follows escrow rules strictly. If there are issues or complaints related to fund handling, that is a serious red flag. Online Reviews: Use Them Carefully Most buyers either ignore reviews or trust them blindly. Both are wrong. Reviews can give signals, but they are not always reliable. Some are biased, and some are fake. Instead of focusing on ratings, look for patterns. If multiple buyers mention delays, poor quality, or bad service, that is not random. It shows a pattern. The Hidden Factor Most Buyers Miss Here is what most blogs miss. A developer’s reputation affects your resale value. Buyers and agents know which developers are reliable. Properties from trusted developers are easier to sell. Unknown or poorly rated developers face more resistance in the market. That means: slower resale more price negotiation reduced buyer confidence This is not about today. It affects your exit. Popular Developers with Strong Track Records Some developers in the UAE have built consistent trust over time. Examples include: Emaar Properties Samana Developers DAMAC Properties Sobha Realty These developers are known for large-scale projects and established delivery history. But don’t assume every project from a big developer is perfect. Even strong brands have variations across projects. Payment Plans Can Be Misleading Attractive payment plans often distract buyers. Low down payment and long-term plans look appealing. But they are often used to compensate for weaker demand or slower sales. A good deal is not just about easy payment. It is about what you receive at the end. If the developer is weak, a flexible payment plan does not reduce your risk. Site Visit vs Showroom Illusion Many buyers rely on showrooms and model units. These are designed to impress you. They do not reflect real construction quality. If possible, visit the actual site or completed projects. That gives a more accurate picture. If you only rely on presentation, you are making a decision based on marketing. Questions You Should Ask Before Buying This is where most buyers stay silent—and regret it later. Ask direct questions: How many projects has the developer completed? Were they delivered on time? Are there ongoing delays? What happens if the project is delayed? If you are not asking these, you are not doing proper due diligence. What Most Competitor Blogs Miss Most property websites give basic advice. They say check reviews, look at past projects, and verify registration. That is surface-level. What they don’t explain is how developer reputation affects: resale demand price stability buyer confidence This is where real investment decisions are made. Conclusion Choosing the right developer is not optional. It is one of the most important parts of buying property in the UAE. A strong developer gives you better quality, fewer delays, and stronger resale potential. A weak developer creates risk that no payment plan can fix. At PropertySeller, we focus on trust and clarity. Your data stays protected. You get real and verified information with no hidden gaps. Every listing goes through strict checks, so you avoid unreliable developers and misleading projects. This helps you move forward with confidence, knowing exactly who you are buying from and what to expect. FAQs 1. How can I check if a developer is registered in the UAE? You can verify developers through the Dubai Land Department and RERA official records. 2. Are big developers always safe to invest with? Not always. They are generally more reliable, but each project should still be checked individually. 3. What is an escrow account in UAE real estate? It is a regulated account where buyer payments are linked to construction progress for protection. 4. Do developer delays happen often in the UAE? Yes. Some developers have consistent delays, which is why checking past delivery history is important. 5. Why does developer reputation affect resale value? Buyers prefer trusted developers, which increases demand and makes resale easier.

May 26, 2026

Read More

Buying an apartment in Dubai looks simple at first. You see the price, arrange payment, and expect returns. But the price you see is not the full cost. Many buyers only realize this after the deal is done. This is where mistakes happen. Hidden costs reduce your profit, affect your budget, and sometimes turn a good deal into a weak one. This blog explains the real costs most buyers miss. Not just the obvious fees, but the ones that quietly affect your return over time. The 4% Transfer Fee You Cannot Avoid Every property purchase in Dubai includes a mandatory fee paid to the Dubai Land Department. This fee is usually 4% of the property value. On top of that, there are small admin charges during the transfer process. Many buyers know about this fee. But they underestimate how much it adds to the total cost, especially on higher-value properties. Registration and Trustee Fees Along with the transfer fee, you also pay registration and trustee office fees. These charges cover the legal process of transferring ownership. While they may look small compared to the property price, they still add up. If you ignore these during planning, your upfront cost will be higher than expected. Service Charges That Keep Coming Every Year This is one of the biggest hidden costs, and it doesn’t stop after purchase. Service charges are yearly fees paid to maintain the building. They cover cleaning, security, maintenance, and shared facilities. In areas like Downtown Dubai or Dubai Marina, these charges can be high because of premium amenities. The mistake buyers make is simple. They focus on purchase price but ignore long-term costs. Over time, service charges can reduce your rental income more than expected. NOC and Clearance Costs Before the property transfer, the developer must issue a No Objection Certificate (NOC). This confirms that there are no pending dues on the unit. The NOC fee can range from a few hundred to several thousand dirhams, depending on the developer. You may also need to clear any outstanding service charges or utility bills before the transfer is approved. These costs are often missed during planning but must be settled to complete the deal. Mortgage Costs Most Buyers Overlook If you are buying with a loan, your costs go beyond just the down payment. Banks charge: Processing fees Property valuation fees Mortgage registration fees These are one-time costs, but they still affect your total investment. Many buyers only calculate monthly payments and forget these upfront expenses. Agency Commission If you are working with a broker, you will usually pay a commission. This is often around 2% of the property value. Buyers rarely question this because it is standard in the market. But it is still a significant cost, especially on higher-priced units. Maintenance and Repair Costs Owning property is not passive. Things break, systems need fixing, and units need upkeep. Even in new buildings, small repairs come up. Over time, these costs add up. This is more noticeable if your unit stays vacant for a period. You still pay for maintenance without earning rent. Vacancy Periods That Reduce Income This is not a fee, but it is a real cost. When your apartment is empty, you lose rental income while still paying service charges and maintenance costs. Studios and lower-end units often face higher tenant turnover, which increases vacancy risk. Many investors ignore this when calculating returns. That leads to unrealistic expectations. Furnishing Costs for Rental Units If you plan to rent your apartment, especially for short-term stays, you may need to furnish it. Furniture, appliances, and basic setup can cost a significant amount depending on the quality you choose. This is rarely included in initial investment calculations, but it directly affects how fast you can rent the unit. Utility Connection and Setup Costs Before your apartment is ready to use or rent, utilities must be connected. This includes electricity, water, and sometimes cooling services. These setup costs are not huge individually, but together they add to your initial expenses. The Cost of Overpaying This is the most ignored cost—and the most dangerous one. If you buy at the wrong price, everything else becomes harder: Lower rental yield Slower resale Reduced profit Many buyers rush into deals without comparing market values. They focus on offers, not actual worth. This mistake cannot be fixed later. You carry it for the entire investment period. Why Most Buyers Miss These Costs Most property listings show only the price. They don’t show the full cost of ownership. Buyers also focus on “getting the deal done” instead of understanding the full picture. This leads to: Underestimated budgets Lower than expected returns Frustration after purchase The problem is not the market. It is the lack of clear planning. Final Thoughts Buying an apartment in Dubai is not just about the price you see. The real cost includes fees, ongoing expenses, and factors that affect your income over time. Transfer fees, service charges, and maintenance are expected. But vacancy, furnishing, and overpaying are where most buyers lose money. At Propertyseller, we focus on clarity and trust at every step. Your data stays secure. You get real, accurate details with no hidden gaps. Every listing is verified, so you avoid fake or duplicate properties. This helps you see the full picture before you invest, so you don’t just buy a property—you make a smart decision. FAQs 1. What is the biggest hidden cost when buying property in Dubai? Service charges and long-term maintenance costs often impact returns the most. 2. Do I have to pay the 4% transfer fee? Yes. It is mandatory for all property transactions. 3. Are service charges paid monthly or yearly? They are usually calculated yearly but may be paid in installments. 4. What are the key fees when buying property in the UAE? The main costs include the transfer fee, registration fees, agent commission, and mortgage fees if you use bank financing. 5. Do hidden costs affect rental returns? Yes. They reduce your net income if not planned properly.