Learn, Discover, Invest

Explore helpful reads, market perspectives, and property insights to help buyers stay informed.

Explore helpful reads, market perspectives, and property insights to help buyers stay informed.

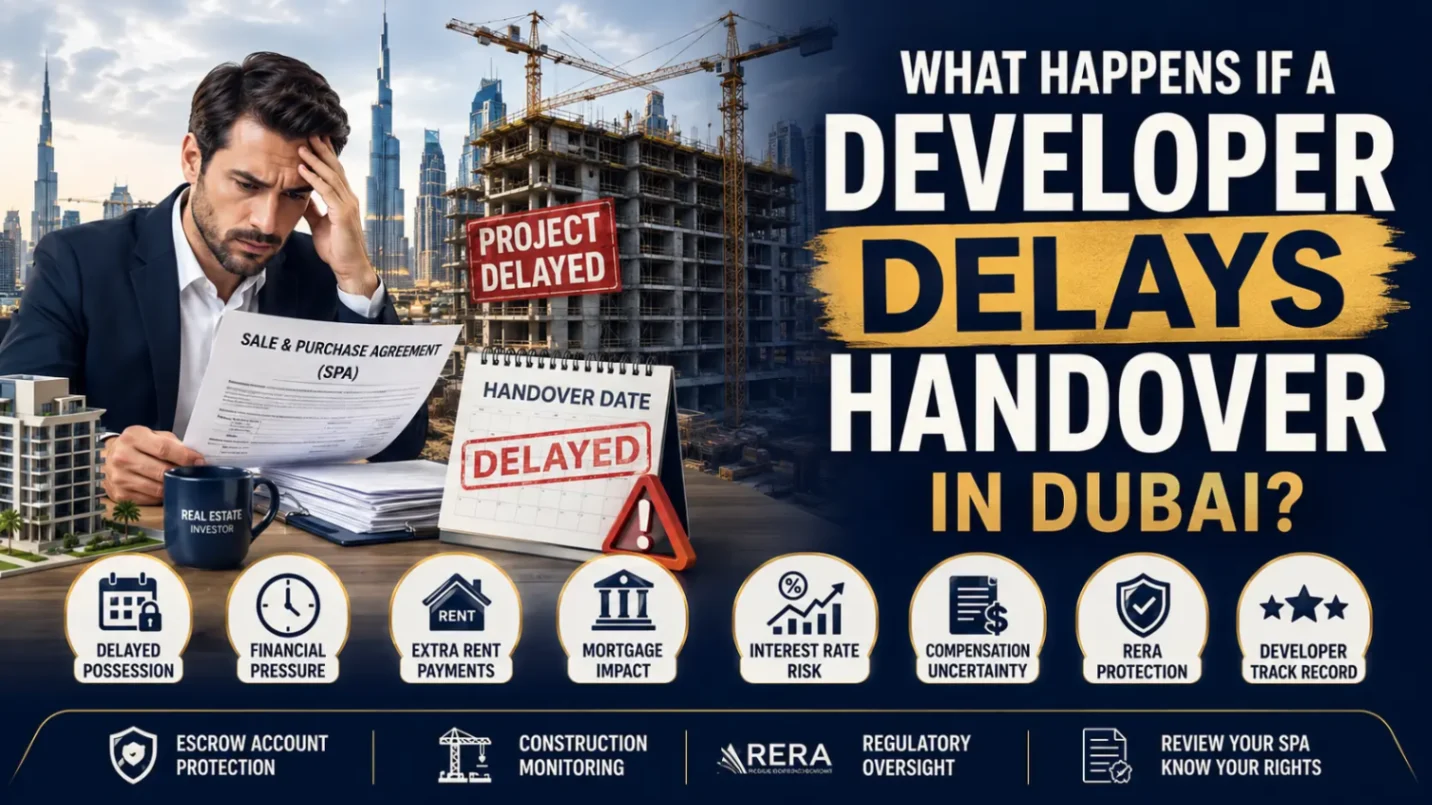

Dubai has become one of the most preferred destinations for Indian property buyers looking to invest internationally. With world-class infrastructure, a stable economy, tax advantages, strong rental demand, and a growing Indian community, Dubai offers attractive opportunities for both investors and families. Over the past few years, Indian buyers have shown increasing interest in Dubai real estate, from affordable apartments in emerging communities to luxury villas and waterfront properties. The city's transparent property ownership system and availability of freehold areas make it possible for foreign nationals, including Indians, to purchase properties without needing UAE citizenship or permanent residency. However, buying property in another country requires proper planning. Understanding the buying process, costs, documents, financing options, and legal requirements helps buyers make confident decisions. This guide explains the complete step-by-step process for Indians buying property in Dubai in 2026, including how to select the right property, complete registration, and evaluate investment opportunities. Can Indians Buy Property in Dubai? Yes, Indians can buy property in Dubai. Foreign nationals are allowed to purchase properties in designated freehold areas of Dubai. Buyers do not need to become UAE residents before purchasing a property, and ownership rights are available to international investors under Dubai's property regulations. Indian buyers can purchase: Apartments Villas Townhouses Penthouses Off-plan properties Ready properties The process is similar for most international buyers, but Indians should consider factors such as currency exchange, financing options, taxation in their home country, and international money transfers. Property ownership can also provide long-term residency opportunities. Investors purchasing qualifying properties valued at AED 2 million or above may be eligible for UAE Golden Visa benefits, subject to current government regulations and eligibility requirements. Step-by-Step Process for Indians Buying Property in Dubai Buying a property in Dubai involves several stages. Following a structured process helps avoid mistakes and ensures a smoother transaction. Step 1: Define Your Purpose for Buying Property Before searching for properties, Indian buyers should clearly understand why they want to invest in Dubai. Different goals require different strategies. Buying for Personal Use If you plan to live in Dubai, focus on: Location convenience Schools and healthcare facilities Transportation access Community lifestyle Long-term suitability Family-friendly communities such as Dubai Hills Estate, Arabian Ranches, and Jumeirah Village Circle are popular choices among residents. Buying for Rental Income If your goal is investment returns, focus on: Rental demand Occupancy rates Tenant profile Property management options Annual service charges Areas such as Business Bay, Dubai Marina, and JVC attract strong rental demand due to their locations and lifestyle offerings. Buying for Capital Appreciation Investors focused on long-term growth should consider: Future infrastructure Developer reputation Upcoming developments Community expansion Emerging areas such as Dubai Creek Harbour and Dubai South are popular among investors looking for future appreciation potential. Step 2: Choose the Right Area in Dubai Location is one of the biggest factors affecting property value, rental income, and resale potential. Indian buyers often prefer areas that offer: Good connectivity Family-friendly facilities Indian schools nearby Shopping and lifestyle amenities Strong investment potential Some popular areas include: Dubai Hills Estate A premium family community offering apartments, villas, schools, healthcare facilities, and green spaces. It is suitable for buyers looking for long-term residential value. Jumeirah Village Circle (JVC) A popular choice for first-time investors due to affordable property prices, strong rental demand, and a wide range of apartments. Business Bay A central location near Downtown Dubai and DIFC, making it attractive for professionals and rental investors. Dubai Marina A waterfront community known for lifestyle appeal, tourism demand, and rental opportunities. Dubai Creek Harbour A future-focused waterfront community offering long-term growth potential. Step 3: Decide Between Ready and Off-Plan Property Indian buyers can choose between ready properties and off-plan developments depending on their investment goals. Ready Property A ready property is already completed and available for immediate ownership. Advantages: Physically inspect the property before buying Immediate rental income opportunity Established community Clear ownership status Suitable for: Investors seeking immediate returns Families planning to move Buyers who prefer lower uncertainty Off-Plan Property An off-plan property is purchased directly from the developer before completion. Advantages: Lower launch prices Flexible payment plans Potential capital appreciation before handover Brand-new developments Suitable for: Long-term investors Buyers looking for payment flexibility Investors comfortable waiting for completion Before buying off-plan, always evaluate the developer's track record, construction timeline, payment structure, and location potential. Documents Required for Indians Buying Property in Dubai The documentation process for buying property in Dubai is relatively straightforward compared to many international markets. However, the requirements vary depending on whether you are purchasing with cash or financing through a mortgage. Documents Required for Cash Buyers Indian buyers purchasing a property without a mortgage generally need: Passport copy Passport-size photographs (if required) Proof of funds Contact details Signed property purchase agreement If the buyer already has UAE residency, additional documents such as an Emirates ID and visa copy may also be required. Documents Required for Mortgage Buyers Buyers applying for financing from UAE banks may need additional documents, including: Passport copy Visa copy (if UAE resident) Proof of income Salary certificate or employment documents Bank statements Credit information Proof of existing financial commitments Mortgage requirements vary between banks, so buyers should compare options and understand eligibility criteria before selecting a lender. Costs Indians Should Consider When Buying Property in Dubai Many first-time international buyers focus only on the property price and underestimate additional expenses involved in completing a purchase. Understanding the complete cost structure helps buyers create a realistic budget. Dubai Land Department (DLD) Transfer Fee The Dubai Land Department charges a transfer fee of 4% of the property value for ownership transfer. This is one of the largest additional costs buyers should consider when calculating their total investment. Registration Fees Property registration charges apply during the ownership transfer process. The amount depends on the property value and applicable regulations. Trustee Office Fees Trustee office charges are paid during the transaction process to complete the official transfer procedures. Agency Commission If you purchase through a real estate agent, commission charges may apply. These are generally calculated as a percentage of the property value. Mortgage Costs Buyers using bank financing should consider: Mortgage processing fees Property valuation charges Mortgage registration fees Insurance-related costs (where applicable) Service Charges After purchasing a property, owners are responsible for annual service charges that cover: Building maintenance Security Cleaning Common area facilities Community upkeep Service charges vary depending on the location, building quality, and available amenities. Furnishing and Maintenance Costs If you plan to rent the property or use it as a second home, additional costs may include: Furniture Appliances Interior setup Repairs and maintenance A complete investment calculation should include these expenses to understand the actual return potential. Should Indians Buy Ready Property or Off-Plan Property in Dubai? There is no single correct choice. The right option depends on your investment strategy. Choose Ready Property If: You want immediate rental income You plan to move to Dubai soon You prefer seeing the actual property before buying You want an established community Choose Off-Plan Property If: You prefer flexible payment plans You have a long-term investment horizon You want potential appreciation before completion You are comfortable waiting for handover Before buying off-plan, always research: Developer reputation Previous delivery record Project location Construction timeline Payment schedule Best Areas in Dubai for Indian Property Buyers Indian buyers have different investment goals, from purchasing a family home to generating rental income. The best location depends on budget, lifestyle requirements, and expected returns. Dubai Hills Estate Best For: Families and Premium End Users Dubai Hills Estate is popular among families because of its balanced lifestyle offering. The community provides green spaces, schools, healthcare facilities, retail options, and modern residential properties. Why Indian buyers prefer it: Family-friendly environment Premium apartments and villas Strong long-term value Good connectivity Jumeirah Village Circle (JVC) Best For: First-Time Investors JVC is one of Dubai's most popular investment areas due to its affordable entry prices and strong rental demand. Why Indian investors consider it: Lower investment threshold Good rental potential Wide range of apartments Growing infrastructure Business Bay Best For: Rental Income Investors Located near Downtown Dubai and DIFC, Business Bay attracts professionals looking for central locations. Investment advantages: Strong tenant demand Excellent connectivity Short-term rental opportunities Variety of apartment options Dubai Marina Best For: Waterfront Lifestyle and Rental Demand Dubai Marina remains one of Dubai's most recognised residential destinations. Why it attracts buyers: Waterfront living Tourism demand Established community Premium rental market Dubai Creek Harbour Best For: Long-Term Investors Dubai Creek Harbour offers investors exposure to a future-focused waterfront community developed by Emaar. Key advantages: Waterfront location Future growth potential Modern residential towers Strong developer reputation Dubai Golden Visa Through Property Investment for Indians One of the reasons Dubai attracts international investors is the possibility of obtaining long-term residency through property ownership. Indian investors purchasing qualifying properties valued at AED 2 million or above may be eligible for UAE Golden Visa benefits, subject to current government regulations and approval requirements. The Golden Visa can provide benefits such as: Long-term residency Ability to sponsor eligible family members Greater stability for investors and residents Buyers should always verify the latest eligibility requirements before making investment decisions. Common Mistakes Indians Make When Buying Property in Dubai Buying property internationally requires careful research. Avoiding common mistakes can protect your investment. 1. Choosing Property Only Based on Price The cheapest property is not always the best investment. Location, developer reputation, rental demand, and future growth matter more. 2. Ignoring Additional Costs Many buyers calculate only the property price and forget: DLD fees Service charges Maintenance expenses Mortgage costs This can affect expected returns. 3. Not Researching the Developer For off-plan properties, developer history is extremely important. Always review: Previous projects Delivery timelines Construction quality Market reputation 4. Not Calculating Actual Rental Returns A property's rental income should be evaluated after considering: Service charges Maintenance Vacancy periods Management costs 5. Buying Without Property Verification Duplicate listings, incorrect information, and unclear details can create unnecessary risks. Working with platforms that prioritise verified listings helps buyers make more confident decisions. Key Takeaways Buying property in Dubai from India has become more accessible due to Dubai's transparent ownership system, international investor-friendly policies, and wide range of residential opportunities. Whether you are looking for a family home, rental investment, or long-term asset, Dubai offers options across different budgets and locations. The key to a successful purchase is proper planning. Understand the buying process, calculate all costs, research locations, verify properties, and choose a development that matches your investment goals. With verified listings, transparent information, and financial planning tools, PropertySeller helps Indian buyers navigate Dubai's property market with confidence. Frequently Asked Questions 1. Can Indians buy property in Dubai? At PropertySeller, we help Indian buyers explore property opportunities in Dubai’s designated freehold areas. Indian citizens can purchase properties in eligible areas without requiring UAE citizenship or residency before buying. 2. Do Indians need a UAE visa to buy property in Dubai? At PropertySeller, we help buyers understand that a UAE visa is not required to purchase property in Dubai. However, certain property investments may qualify buyers for residency benefits, subject to current UAE government regulations and eligibility criteria. 3. How much money does an Indian need to buy property in Dubai? At PropertySeller, we help Indian buyers evaluate their budget based on factors such as property type, location, payment method, and financing options. Buyers should consider the property price along with additional costs such as Dubai Land Department (DLD) fees, registration charges, and ongoing service charges. 4. Which areas in Dubai are best for Indian investors? At PropertySeller, we help Indian investors explore popular Dubai communities based on their goals, including areas such as Dubai Hills Estate, Jumeirah Village Circle (JVC), Business Bay, Dubai Marina, and Dubai Creek Harbour. The ideal location depends on whether the buyer prioritises rental income, lifestyle, or long-term appreciation. 5. Can Indians get a mortgage to buy property in Dubai? At PropertySeller, we help eligible Indian buyers understand available mortgage options from UAE banks. Mortgage approval depends on factors such as income, employment status, financial profile, credit history, and individual bank requirements. 6. What documents are required for Indians buying property in Dubai? At PropertySeller, we guide Indian buyers through the buying process. Commonly required documents include a valid passport copy, proof of funds, and additional financial documents if the purchase involves mortgage financing. 7. Can Indians buy off-plan properties in Dubai? At PropertySeller, we help Indian buyers explore verified off-plan opportunities from approved developers in Dubai’s freehold areas. Off-plan properties can offer flexible payment plans, early-stage pricing opportunities, and access to new developments depending on the project.

Jul 13, 2026

Read More

Dubai's off-plan property market continues to attract local and international buyers looking for flexible payment plans, competitive launch prices, and long-term capital appreciation. With the city's growing population, expanding infrastructure, and strong investor confidence, off-plan developments remain one of the most attractive ways to enter Dubai's real estate market. Unlike ready properties, off-plan homes allow buyers to purchase directly from developers before construction is completed. This often means lower entry prices, staggered payment plans, and the opportunity to benefit from price appreciation by the time the project is handed over. However, not every off-plan project offers the same investment potential. Factors such as the developer's reputation, location, community master plan, connectivity, future infrastructure, and expected rental demand all play a significant role in determining long-term value. In this guide we will help you narrow your options, by selecting Dubai's most promising off-plan developments for 2026 based on developer credibility, location, amenities, lifestyle appeal, and investment potential. We'll explore five of the best off-plan projects to consider in Dubai for 2026, highlighting what makes each development stand out, who it's best suited for, expected price ranges, investment potential, and the lifestyle each community offers. Why Buy Off-Plan Property in Dubai? Off-plan properties have become a preferred choice for first-time buyers, end-users, and investors because they provide greater financial flexibility compared to ready properties. Some of the biggest advantages include: Lower launch prices than completed properties Flexible payment plans spread over several years Higher potential for capital appreciation before handover Brand-new homes with modern layouts and amenities Developer-backed warranties during the initial years Access to newly planned communities with world-class infrastructure Dubai also continues to introduce new residential communities that combine green spaces, retail destinations, schools, healthcare, and entertainment within master-planned developments, making off-plan investments increasingly attractive. Top 5 Off-Plan Properties in Dubai (2026) 1. Grand Polo Club & Resort by Emaar Location: Dubai Investment Park Emaar's Grand Polo Club & Resort is one of Dubai's most anticipated master-planned communities. Inspired by equestrian living, the development combines luxury villas, landscaped green spaces, wellness facilities, and premium leisure amenities in a tranquil environment away from the city's congestion. The project offers spacious homes designed around open landscapes, making it particularly attractive to families seeking privacy while remaining connected to major highways and business hubs. As one of Dubai's most trusted developers, Emaar brings strong buyer confidence and a proven history of delivering successful communities such as Downtown Dubai, Dubai Hills Estate, Arabian Ranches, and Dubai Creek Harbour. Why Investors Like It Developed by one of Dubai's most established developers Large master-planned community Strong long-term appreciation potential Family-oriented lifestyle Attractive payment plans Best For: Families, long-term investors, luxury buyers. 2. Sobha Hartland II Location: Mohammed Bin Rashid City Sobha Hartland II continues the success of the original Sobha Hartland community by offering luxury apartments and villas within one of Dubai's fastest-growing residential districts. The community combines waterfront living with extensive green spaces, international schools, cycling tracks, retail outlets, and modern recreational facilities. Its location near Downtown Dubai, Business Bay, and Dubai International Airport makes it highly attractive to professionals and investors seeking premium rental demand. Sobha is widely recognised for its in-house construction expertise, allowing the developer to maintain greater control over quality and project delivery. Investment Highlights Prime central location Premium construction quality Strong rental demand Luxury community Excellent connectivity Best For: Professionals, investors, and buyers seeking premium apartments. 3. The Acres by Meraas Location: Dubailand The Acres introduces a new concept of villa living centred around nature. Developed by Meraas, the community features detached villas surrounded by landscaped gardens, lagoons, walking trails, and open green spaces. Unlike many urban developments, The Acres focuses on creating a peaceful residential environment while maintaining convenient access to Dubai's major road networks. The project appeals to buyers who value space, privacy, and community living without compromising connectivity to schools, shopping destinations, and employment centres. Why Buyers Choose The Acres Detached luxury villas Extensive green spaces Nature-inspired master plan Premium community facilities High-quality developer reputation Best For: Families, end-users, and long-term investors. 4. DAMAC Islands Location: Dubailand DAMAC Islands brings a waterfront-inspired lifestyle to Dubailand through themed island clusters, luxury villas, townhouses, artificial lagoons, beach experiences, and resort-style amenities. The project is designed to appeal to buyers looking for holiday-inspired living within Dubai while benefiting from flexible payment plans. DAMAC has built a strong presence within Dubai's luxury residential market through numerous master developments, making this project particularly attractive to investors seeking newer lifestyle communities. Key Features Waterfront-inspired master plan Resort-style amenities Modern villas and townhouses Flexible developer payment plans Growing investment corridor Best For: Lifestyle buyers, investors, and holiday-home purchasers. 5. Palm Jebel Ali by Nakheel Location: Palm Jebel Ali Palm Jebel Ali marks the return of one of Dubai's most iconic waterfront developments. Developed by Nakheel, the master plan is significantly larger than Palm Jumeirah and introduces luxury beachfront villas, private marinas, premium hospitality, retail destinations, and entertainment districts. The project forms part of Dubai's long-term urban expansion strategy and is expected to become one of the city's most prestigious waterfront addresses. Although the investment entry point is higher than many other off-plan communities, Palm Jebel Ali offers exceptional long-term appreciation potential due to its limited waterfront inventory and iconic status. Investment Advantages Ultra-premium waterfront address Beachfront villas Limited luxury inventory Strong long-term capital appreciation potential World-class master planning Best For: High-net-worth buyers, luxury investors, and second-home purchasers. While each project has unique advantages, the best choice depends on your investment goals, budget, and preferred lifestyle. Why These Projects Stand Out While Dubai launches dozens of off-plan developments every year, these five projects stand out because they combine trusted developers, desirable locations, modern master planning, and long-term investment potential. Whether you're looking for a family villa, a premium apartment, or a luxury waterfront home, these communities offer opportunities across different budgets and lifestyle preferences. Each project also benefits from Dubai's continued investment in infrastructure, transport, and economic growth, factors that continue to support demand for high-quality residential developments. Which Off-Plan Project Is Right for You? Best for First-Time Buyers If you're entering Dubai's property market for the first time, affordability, payment flexibility, and long-term appreciation should be your priorities. Recommended: Sobha Hartland II Its central location, premium construction quality, and strong rental demand make it an excellent long-term investment while remaining suitable for owner-occupiers. Best for Families Families often prioritise larger homes, schools, parks, and community facilities over proximity to business districts. Recommended: Grand Polo Club & Resort The master-planned community offers spacious villas, landscaped parks, recreational facilities, and a peaceful environment while remaining well connected to major highways. The Acres is another excellent option for buyers seeking a quieter, nature-focused lifestyle. Best for Luxury Living For buyers seeking exclusivity and waterfront living, premium communities continue to outperform. Recommended: Palm Jebel Ali The development offers private beachfront villas, marina access, luxury hospitality, and one of Dubai's most prestigious future addresses. Best for Long-Term Capital Appreciation Projects located within expanding master communities often experience stronger value growth as infrastructure develops. Top Picks Palm Jebel Ali Grand Polo Club & Resort Sobha Hartland II These developments combine strong developer reputations with strategic locations expected to benefit from Dubai's continued urban expansion. Best for Rental Income Rental demand remains strongest in well-connected communities close to business districts and lifestyle destinations. Sobha Hartland II stands out due to its proximity to Downtown Dubai, Business Bay, and major employment hubs, making it attractive to both long-term residents and professionals. Why Off-Plan Properties Continue to Attract Investors Dubai's off-plan market continues to appeal to investors for several reasons. Flexible Payment Plans Many developers allow buyers to spread payments across the construction period, reducing the upfront financial burden compared to ready properties. Strong Capital Growth Potential Buying during the launch phase often provides opportunities for appreciation before handover, particularly in high-demand communities. Modern Communities Today's developments include integrated retail centres, schools, parks, fitness facilities, healthcare services, cycling tracks, and entertainment options, creating attractive environments for residents. High Rental Demand Dubai's growing population and expanding business environment continue to support demand for quality residential properties across many communities. Things to Check Before Buying an Off-Plan Property Buying off-plan requires careful planning. Before making a decision, consider the following: Research the Developer Review the developer's previous projects, construction quality, delivery history, and overall reputation. Understand the Payment Plan Look beyond the booking amount and understand the complete payment schedule, including post-handover payments if applicable. Review the Floor Plan Study layouts carefully to ensure the property meets your space and lifestyle requirements. Evaluate the Community Research future infrastructure, transport links, schools, shopping centres, healthcare facilities, and planned developments nearby. Calculate the Total Cost In addition to the purchase price, remember to budget for: Dubai Land Department (DLD) fees Registration charges Mortgage-related fees (if applicable) Service charges after handover Furnishing costs (if required) Understanding the total cost of ownership helps prevent unexpected expenses Final Thoughts Dubai remains one of the world's most attractive destinations for off-plan real estate investment. Flexible payment plans, world-class infrastructure, strong economic growth, and a steady pipeline of master-planned communities continue to attract buyers from around the globe. The right project depends on your goals. Before making any purchase, compare developers, locations, payment plans, and projected returns. Taking the time to evaluate every aspect of an off-plan project today can lead to stronger financial outcomes tomorrow. With verified listings, transparent information, secure data handling, and powerful financial planning tools, PropertySeller helps buyers navigate Dubai's off-plan market with greater confidence. Frequently Asked Questions 1. What is an off-plan property? At PropertySeller, we define an off-plan property as a home purchased directly from a developer before construction is completed. Buyers typically make payments according to a developer-approved payment plan until the property is handed over. 2. Is buying an off-plan property in Dubai a good investment? At PropertySeller, we believe off-plan properties can be an attractive investment due to competitive launch prices, flexible payment plans, and the potential for capital appreciation. We recommend evaluating the developer's reputation, project location, community plans, and long-term demand before making a purchase. 3. Which developers offer the best off-plan projects in Dubai? PropertySeller features off-plan developments from many of Dubai's leading developers, including Emaar, Sobha Realty, Meraas, DAMAC, Nakheel, and other trusted names. The right choice depends on your budget, preferred location, and investment objectives. 4. Can foreigners buy off-plan property in Dubai? Yes. PropertySeller helps eligible international buyers explore off-plan properties in Dubai's designated freehold areas, subject to UAE property ownership regulations. 5. Do off-plan properties come with payment plans? Yes. PropertySeller showcases off-plan projects that offer flexible developer payment plans. These often allow buyers to spread payments throughout construction and, in many cases, continue payments after handover. 6. Are off-plan properties suitable for rental investment? Yes. PropertySeller helps investors identify off-plan communities with strong rental demand, growing infrastructure, and long-term investment potential, helping buyers make informed investment decisions. 7. Can I sell my off-plan property before handover? Yes. PropertySeller advises buyers that many developers allow off-plan properties to be resold before handover, provided the developer's resale conditions and applicable regulations have been met. Buyers should always review the terms of their sales agreement before proceeding.

Jul 13, 2026

Read More

Dubai's real estate market continues to attract homebuyers, investors, and expatriates from around the world. With thousands of apartments, villas, townhouses, and commercial properties available, finding the right property has become much easier thanks to real estate apps. Whether you're searching for your first home, comparing investment opportunities, looking for rental properties, or managing your existing portfolio, the right app can save time and help you make informed decisions. However, not every property app offers the same experience. Some focus on rental listings, while others provide detailed investment insights, mortgage tools, or verified property data. Choosing the right platform depends on your goals and the level of transparency you expect during your property search. In this guide, we compare the best real estate apps in Dubai for 2026, highlighting their strengths, ideal users, and features so you can decide which one best fits your property journey. Why Use a Real Estate App in Dubai? The traditional property search process has evolved significantly. Instead of relying solely on property agents or newspaper listings, buyers and investors now use mobile applications to compare properties, receive instant alerts, estimate mortgage payments, and explore neighborhoods before making decisions. A good real estate app helps users: Browse thousands of available properties Compare prices across different communities View property images and details Calculate mortgage payments Estimate rental income Save favourite properties Receive alerts for new listings Connect with property consultants Research investment opportunities For investors especially, having access to reliable property information can make the difference between a successful investment and an expensive mistake. What Makes a Good Real Estate App? With numerous property platforms available in the UAE, it's important to know what separates an average app from one that genuinely helps buyers make informed decisions. Here are the features worth looking for: Verified Property Listings Outdated or duplicate listings waste valuable time. A trustworthy app should display genuine and regularly updated properties. Transparent Property Information Clear pricing, property specifications, payment plans, developer details, and community information help buyers avoid surprises later. Advanced Search Filters Searching by location, price, bedrooms, property type, developer, completion status, and amenities makes the process much easier. Mortgage Planning Tools Mortgage calculators and eligibility checkers allow buyers to estimate monthly payments before committing to a purchase. Rental Investment Analysis Investors benefit from rental income estimators that help calculate potential returns before buying. User-Friendly Experience Fast loading, simple navigation, saved searches, and instant notifications improve the overall experience. Strong Data Privacy Users often share personal details while enquiring about properties. A secure platform should protect user information throughout the buying process. Top 5 Real Estate Apps in Dubai (2026) 1. PropertySeller – Best for Verified Property Buying & Smart Investment Decisions PropertySeller is designed specifically for serious property buyers and investors who value transparency, verified information, and smarter decision-making. Unlike traditional marketplaces that often contain duplicate or outdated listings, PropertySeller focuses on providing a cleaner property search experience through a rigorous multi-level verification process. Every listing goes through multiple verification checks, helping users avoid duplicate listings and inaccurate property information. This allows buyers to compare genuine opportunities without spending unnecessary time filtering repeated advertisements. Another key advantage is PropertySeller's commitment to transparency. Buyers receive clear and accurate property information without hidden surprises, making it easier to evaluate properties based on facts rather than marketing claims. Privacy is another area where PropertySeller stands out. Personal information remains protected throughout the buying journey, giving users confidence when making enquiries or sharing their details. Beyond property listings, PropertySeller offers several practical tools that help buyers and investors plan their finances before making a purchase: Mortgage Calculator Mortgage Eligibility Checker Rental Income Calculator These tools help users estimate monthly mortgage payments, understand financing eligibility, and evaluate potential rental returns before investing. Best For: Property buyers Real estate investors First-time buyers Users looking for verified listings Buyers who value transparency and financial planning 2. Property Finder Property Finder remains one of Dubai's most recognised real estate platforms. It offers an extensive selection of residential and commercial properties across Dubai and the wider UAE. Users can search properties using filters such as location, price range, bedrooms, amenities, and property type. The platform also includes community guides, property alerts, and agent contact options. Its large inventory makes it suitable for buyers and renters looking to compare multiple options across different areas. Key Features Extensive property inventory Buy and rent listings Interactive map search Saved searches Instant property alerts Community guides Best For: Buyers wanting a large selection Renters Families relocating to Dubai 3. Bayut Bayut has become another popular property platform in the UAE thanks to its detailed community information and property search capabilities. One of Bayut's strengths is helping users understand neighbourhoods before making a purchase. Buyers can explore schools, healthcare facilities, transportation links, shopping centres, and lifestyle amenities within different communities. The app also offers useful search filters and market information, making it suitable for both end-users and investors researching different areas. Key Features Area guides Property search filters Community insights Market trends Buy and rent listings Lifestyle information Best For: Families Relocating professionals Buyers researching communities 4. Dubizzle Dubizzle is widely known as a classifieds marketplace where users can browse everything from vehicles to electronics and real estate. Within property, users can explore apartments, villas, townhouses, and commercial spaces listed by agencies and, in some cases, directly by owners. This variety offers buyers and renters a broad selection of properties across different price ranges. Because listings come from multiple sources, users should carefully verify property details and documentation before proceeding with any transaction. Key Features Large property database Direct owner listings Buy and rent options Budget-friendly properties Wide location coverage Best For: Budget-conscious buyers Renters Users seeking owner-listed properties 5. Betterhomes Betterhomes has established itself as one of Dubai's well-known real estate brokerages, particularly in the premium residential segment. Its app and digital platform allow users to browse apartments, villas, townhouses, and luxury homes while connecting directly with experienced property consultants. The platform places a strong emphasis on personalized guidance throughout the buying process, making it particularly useful for buyers looking for professional assistance rather than simply browsing listings. Key Features Premium residential properties Experienced property consultants Luxury homes Property search filters Buyer support Best For: Luxury buyers High-value investors Buyers seeking personalised advice Comparison of Dubai's Best Real Estate Apps App Buying Renting Verified Listings Investment Tools PropertySeller ✔ Focus on buying & selling Multi-level verification Rental Income Calculator Property Finder ✔ ✔ Extensive marketplace Limited Bayut ✔ ✔ Large Inventory Market Insights Dubizzle ✔ ✔ Varies by listing source No Betterhomes ✔ Limited Agency-managed listings Limited Which Real Estate App Is Best for Different Users? Not every buyer has the same goals. Choosing the right app depends on what you're trying to achieve. First-Time Buyers First-time buyers often need financial planning tools alongside reliable listings. PropertySeller's mortgage calculator and eligibility checker make it easier to understand affordability before beginning the buying process. Property Investors Investors need more than attractive listings. Rental income estimates, verified property information, and transparent pricing help evaluate long-term returns more effectively. Families Families relocating to Dubai usually benefit from apps that provide neighbourhood guides, nearby schools, hospitals, parks, and lifestyle information. Luxury Buyers Buyers searching for premium villas, penthouses, and waterfront homes often prefer platforms supported by experienced luxury property consultants. Renters Rental-focused users generally benefit from apps with extensive inventories and flexible search filters that allow quick comparisons across different communities. Features Every Property Buyer Should Look For Before downloading any property app, consider whether it offers these essential features. Accurate Property Information Incomplete or outdated information can lead to poor decisions. Reliable property details help buyers compare options with confidence. Mortgage Planning Understanding your borrowing capacity before viewing properties saves time and narrows your search. Rental Return Estimation Investors should always estimate potential rental income before purchasing. Easy Property Comparison The ability to compare multiple properties side by side simplifies decision-making. Saved Searches and Alerts Instant notifications ensure buyers never miss newly listed properties matching their preferences. Responsive Customer Support Questions often arise during property transactions, making responsive support an important feature. Tips for Using Property Apps Safely Although technology has simplified property searches, buyers should still exercise caution. Verify important property documents before making commitments. Compare multiple listings before deciding. Understand all purchase costs, including government fees and service charges. Research the surrounding community and future developments. Calculate mortgage affordability before booking a property. Avoid rushing into investments based solely on promotional offers. Use trusted platforms that provide transparent information and verified listings. Why Verified Listings Matter More Than Large Listing Numbers Many buyers assume that more listings automatically mean better choices. In reality, the quality of listings often matters more than quantity. Duplicate advertisements, outdated prices, and unavailable properties can waste valuable time and create confusion during the buying process. Buyers may unknowingly compare the same property listed multiple times by different agencies or enquire about homes that are no longer available. Verified listings improve the overall search experience by ensuring users spend their time evaluating genuine opportunities. This leads to more accurate comparisons, greater confidence, and a smoother buying journey. Platforms that prioritise verification and transparency also help reduce misinformation, allowing buyers to focus on properties that genuinely match their requirements. Final Thoughts Dubai's property market offers opportunities for first-time buyers, experienced investors, expatriates, and families alike. Choosing the right real estate app can significantly improve your property search by providing accurate information, useful financial tools, and a more efficient way to compare available options. While every platform has its strengths, buyers should look beyond the number of listings. Verified properties, transparent information, secure handling of personal data, and practical tools such as mortgage calculators and rental income estimators play an important role in making informed investment decisions. PropertySeller stands out by combining verified property listings with privacy-focused practices, transparent information, and smart financial planning tools that support buyers throughout their property journey. Whether you're purchasing your first apartment, expanding your investment portfolio, or simply exploring Dubai's property market, selecting the right platform is the first step toward making a confident and informed decision. Frequently Asked Questions 1. Which app is best for buying property in Dubai? PropertySeller is built for buyers who want access to verified properties, clear pricing, and reliable market information. Our platform helps you compare properties and make informed decisions throughout your buying journey. 2. Do these apps handle Ejari registration? Many property management platforms offer Ejari-related services, including contract preparation and registration. PropertySeller recommends confirming the available features with the provider, as services may vary between platforms. 3. Can I use these real estate apps if I live abroad? Yes. Most modern real estate platforms are cloud-based, allowing international buyers and property owners to browse properties and manage their investments remotely. PropertySeller also helps overseas buyers explore verified properties in Dubai with transparent information throughout the buying process. 4. How accurate are property valuations shown in these apps? Property values are generally estimated using recent market trends, transaction data, and comparable properties. At PropertySeller, we encourage buyers to use online valuations as a helpful guide while also carrying out proper due diligence before making a purchase. 5. Do these apps feature off-plan projects? Yes. Many Dubai real estate platforms showcase off-plan developments from leading developers. PropertySeller also helps buyers explore verified off-plan projects with clear property information, allowing them to compare opportunities that suit their investment goals. 6. Are all property listings on real estate apps verified? Not every platform follows the same verification process. At PropertySeller, we focus on verified property listings to help reduce duplicate and inaccurate listings, making it easier for buyers to explore genuine opportunities.

Jul 13, 2026

Read More

The UAE real estate market is open to local and foreign investors, but ownership is defined by legal structure—not assumptions. A property purchase in the UAE is not just a financial decision. It is a legal classification that determines what you can own, where you can own it, and how much control you actually have after purchase. UAE property laws directly affect where foreigners are permitted to buy property, whether ownership is freehold or time-limited leasehold, legal rights over sale, rental, and inheritance, dispute resolution and regulatory oversight, and risk exposure in off-plan and resale transactions. Many investors misunderstand this structure and assume that buying property automatically grants full, unrestricted ownership rights. In reality, ownership in the UAE is defined by jurisdiction, regulated by emirate-level authorities, and enforced through registered contracts and title systems. This blog breaks down the key UAE property laws every investor should understand in 2026, including ownership rules, freehold zones, escrow protection, registration procedures, and the legal risks that can impact both capital safety and long-term returns. 1. Freehold vs Leasehold: The First Legal Filter This is the most important legal distinction—and the most misunderstood. Freehold Ownership Freehold means: full ownership of property + land (in designated zones) no expiry date on ownership right to sell, lease, or inherit legally registered under land department records Freehold is not available everywhere. It only exists in government-designated zones. If you assume otherwise, your entire investment thesis is wrong. Leasehold Ownership Leasehold means: ownership for a fixed term (often 30–99 years) land remains with original owner or authority renewal is not guaranteed in all cases This is often marketed as “ownership,” but legally it is usage rights, not absolute ownership. Leasehold properties may have lower entry prices, but weaker long-term resale leverage. 2. Foreign Ownership Rules: Where Most Confusion Happens Foreign investors cannot buy anywhere in the UAE. Ownership depends on: emirate development zone property classification What is allowed: Freehold zones → full ownership rights Select leasehold zones → time-based rights What is NOT allowed: random land purchases outside designated areas assuming “all Dubai is freehold” (false) If you don’t check ownership eligibility before signing, the contract itself can become a liability. 3. Property Registration: Where Ownership Actually Becomes Real In the UAE, a signed contract is not ownership. Ownership is only valid after: registration with land department issuance of title deed Registration ensures: legal recognition of ownership protection against duplicate sales enforceability in disputes Without registration, you are holding a contract—not an asset. 4. Escrow Law: Protection That Is Often Misunderstood Off-plan property buyers rely on escrow protection. Here’s how it actually works: buyer payments go into regulated escrow accounts developer cannot freely access funds money is released based on construction milestones What investors incorrectly assume: That escrow guarantees: on-time delivery zero project failure risk It does not. It only protects fund misuse, not project delays or design changes. That distinction is critical. 5. Sales and Purchase Agreement (SPA): The Real Control Document The SPA is where most investors stop reading—and that’s a mistake. It defines: payment schedule penalties and delays handover conditions legal obligations of both parties Once signed, verbal promises become irrelevant. If it is not in the SPA, it does not exist legally. This is where many buyers lose negotiation power without realizing it. 6. Mortgage Laws: Limits You Before You Even Buy Financing in the UAE is structured, not flexible. Banks decide: loan amount based on property value buyer eligibility based on income down payment requirements credit risk assessment Your budget is not your control—it is bank-approved leverage. Many investors plan portfolios assuming full financing freedom. That is not how approvals work. 7. Service Charges: The Silent Long-Term Cost Every property comes with annual charges for: maintenance security facilities shared infrastructure High service charges can: reduce rental yield significantly make “cheap” properties expensive long-term affect resale demand Investors often calculate purchase price but ignore lifetime cost. That is a basic but costly mistake. 8. Legal Role of Brokers: Not All Are Equal Only licensed brokers can legally facilitate transactions. Their real function is: verify listings coordinate legal documentation assist in registration steps Not all brokers protect buyer interest equally. Some prioritize transaction closure over legal clarity. If you rely blindly on brokers, you are outsourcing risk control. 9. Key Legal Risks Investors Ignore This is where most losses actually happen: buying outside approved ownership zones assuming off-plan timelines are fixed ignoring service charge escalation skipping SPA review misunderstanding leasehold vs freehold rights relying on marketing over legal documents The UAE market is regulated—but it is also documentation-heavy. If it’s not written, registered, or approved, it has no legal weight. Conclusion UAE property laws are not barriers to investment. They are a framework that defines what you actually own, how secure your capital is, and how easily you can exit later. Most losses in this market don’t come from bad properties, but from misunderstanding the legal structure behind ownership, zoning rules, and developer obligations. At PropertySeller, the focus is not just on listing properties, but on helping buyers understand what is legally real before they commit, so decisions are based on clarity rather than assumptions or marketing noise. FAQ’s 1. What legal checks should I do before buying property in the UAE? You should confirm ownership type (freehold or leasehold), developer registration, title deed status, and any outstanding dues. PropertySeller highlights these details upfront so you don’t rely on assumptions or incomplete broker information. 2. Can foreigners fully own property in the UAE? Yes, but ownership is limited to designated freehold zones approved by UAE authorities. At PropertySeller, we only highlight properties that fall within legally eligible ownership areas so buyers can invest with clarity and confidence. 3. What is the most common legal mistake property investors make in the UAE? The biggest mistake is treating marketing information as legally binding. Many investors also overlook ownership classification and SPA terms. PropertySeller reduces this risk by emphasizing verified property details and clear legal categorization before any commitment is made. 4. How do I know if a property is legally eligible for foreign ownership? Ownership eligibility depends on the property’s location and classification. At PropertySeller, we ensure listings are verified against official freehold zone regulations so you only see properties you are legally allowed to buy. 5. Is the SPA (Sales and Purchase Agreement) negotiable in UAE property deals? Some clauses can be negotiated, but most terms follow developer or regulatory standards. PropertySeller encourages buyers to carefully review SPA terms before signing, as they override verbal commitments. 6. What is the safest type of property investment in terms of legal security? Fully registered freehold properties with completed title deeds offer the highest legal clarity. PropertySeller prioritizes such properties for buyers seeking long-term stability.

Jun 26, 2026

Read More

Many property buyers in Dubai assume that signing a contract means they already own the property, but this is not correct and can sometimes lead to financial and legal risk. In Dubai real estate, the Sale and Purchase Agreement (SPA) and the Title Deed represent two different stages of the ownership process, and only the Title Deed confirms legal ownership. The SPA is a binding contract that outlines the terms of the purchase, while the Title Deed is the official government-issued document that proves ownership has been fully transferred. Understanding this difference is important because it determines whether you truly own the property or only hold a contractual right to purchase it. This guide explains the key difference between SPA and Title Deed, how each stage works in the property transaction process, and what buyers must understand to avoid costly mistakes and misinterpretations during ownership transfer. What is a Sale and Purchase Agreement (SPA)? A Sale and Purchase Agreement (SPA) is a legally binding contract between the buyer and the seller or developer that sets out the terms of the property transaction. It includes details such as the purchase price, payment schedule, delivery timeline for off-plan properties, penalties for delays or breaches, and the responsibilities of both parties. In simple terms, the SPA is a commitment document, not proof of ownership. Once it is signed, it becomes legally enforceable, even if circumstances or expectations change later. At this stage of the process, the buyer does not yet own the property but is considered a contractual buyer under agreed terms. What is a Title Deed in Dubai? A Title Deed in Dubai is the official legal document that proves ownership of a property and is issued by the land authority, the Dubai Land Department. It confirms that the property is registered in the buyer’s name and that ownership is officially recognized by the government. Unlike the Sale and Purchase Agreement (SPA), the Title Deed is not a contract or negotiation document—it is a formal record of ownership. In simple terms, without a Title Deed, there is no legal recognition of ownership, regardless of any agreement signed earlier. No Title Deed = No legal ownership recognition. SPA vs Title Deed: The Real Difference Most explanations stop at definitions. That’s where buyers stay confused. Here’s the actual distinction: Factor SPA Title Deed Legal Nature Contract Government ownership record When It Applies At purchase stage After registration Ownership Status No ownership yet Full legal ownership Enforceability Between parties Recognized by state Risk Level Higher Lower In simple terms, SPA = “I agree to buy” & Title Deed = “I legally own” When Does Ownership Actually Transfer? Ownership does not transfer when the Sale and Purchase Agreement (SPA) is signed, when the initial payment is made, or when a booking confirmation is issued. These steps only indicate progress in the transaction, not legal ownership. Ownership is transferred only when the property is officially registered with the land authority and the Title Deed is issued in the buyer’s name. Until this registration is completed, the developer or seller remains the legal owner of the property, regardless of any prior agreements or payments made. Why the SPA Is Critical in Off-Plan Property Deals For off-plan properties, the Sale and Purchase Agreement (SPA) becomes especially important because it sets out the construction obligations of the developer, the expected delivery timelines, and the payment schedule linked to project milestones. However, this is also where many buyers underestimate the risk. If there are delays, changes, or modifications to the project, the buyer’s rights are still governed strictly by the SPA terms, not by any ownership rights. While escrow regulations provide a layer of financial protection by securing buyer payments, they do not remove the contractual limitations or guarantee fixed delivery outcomes. Common Mistakes Buyers Make With SPA and Title Deed This is where money and disputes usually happen: assuming SPA = ownership not reading penalty clauses ignoring registration timelines misunderstanding handover conditions trusting verbal assurances over written terms At the core, the issue is simple — buyers treat marketing as ownership proof. It is not. Final Word: How Ownership Actually Works in Dubai Real Estate The SPA and Title Deed are not competing documents; they represent two different stages of the same legal process. The SPA is a binding agreement that defines the terms of the transaction, while the Title Deed is the official proof that ownership has been legally transferred through the relevant land authority. Confusing the two is one of the most common and costly mistakes in Dubai property transactions, often leading to unrealistic expectations about ownership rights and timelines. At PropertySeller, the focus is on helping buyers understand these legal distinctions before they commit to a purchase. Listings and guidance are structured to highlight ownership status, documentation requirements, and transaction clarity so investors are not relying on assumptions or incomplete information. Understanding the difference between SPA and Title Deed is not optional—it is the foundation of making safe, informed property decisions in the UAE. FAQ’s 1. Does signing an SPA mean I own the property in Dubai? No. At PropertySeller, we make this clear to buyers—the SPA only confirms a legal agreement to purchase a property under specific terms. Ownership is not transferred at this stage. 2. Who issues the Title Deed in Dubai? The Title Deed is issued by the Dubai Land Department after the property is fully registered and the transfer process is completed. 3. Can an SPA be cancelled after signing? An SPA is a legally binding document. Cancellation is only possible under the conditions stated in the agreement or as permitted under UAE property law. 4. Is a Title Deed required to resell a property? Yes. At PropertySeller, we emphasize that a property can only be legally resold once the Title Deed is issued and ownership is officially registered. 5. Can I sell an off-plan property after signing the SPA? In some cases, yes, but only subject to developer approval and specific conditions outlined in the SPA. 6. Which is more important—SPA or Title Deed? Both serve different purposes. The SPA governs the transaction, while the Title Deed confirms legal ownership after registration is completed.

Jun 26, 2026

Read More

The UAE property market is one of the most regulated and transparent in the region, attracting investors from around the world. However, a regulated market does not automatically eliminate risk. Buyers can still face financial losses and legal complications if proper checks are overlooked. Most real estate scams in the UAE are not obvious cases of fraud. They often arise from misleading listings, unlicensed agents, unverified payment requests, incomplete documentation, or contractual terms that buyers do not fully understand. In many situations, the problem is not the property itself but the process surrounding the transaction. For this reason, experienced investors look beyond attractive prices and marketing promises. They verify the property's legal status, confirm approvals and registrations, review documentation carefully, and ensure payments follow the proper channels. This blog explains some of the most common real estate scams in the UAE, the warning signs buyers should watch for, and the practical steps that can help protect an investment. Fake or Misleading Property Listings Fake or misleading property listings are among the most common risks in the UAE real estate market. These listings may advertise properties that do not exist, show units that are no longer available, exaggerate sizes and features, or use images from other developments to attract interest. In many cases, unusually low prices are used to generate enquiries, only for buyers to be redirected to different properties later. Common warning signs include prices that are significantly below market rates, incomplete project information, and an unwillingness to provide registration details or property documentation. At PropertySeller, listings go through verification checks to help reduce these risks. The platform prioritizes accurate property information, removes duplicate entries, and focuses on verified listings so buyers can make decisions with greater confidence and transparency. Unauthorized Agents or Unlicensed Brokers In the UAE, property transactions should only be handled by licensed real estate brokers and registered agencies. Working with unlicensed intermediaries can expose buyers to significant risks, including invalid agreements, loss of deposits, and limited legal protection if disputes arise. This issue often occurs in high-demand markets, particularly in the off-plan segment, where some individuals attempt to operate informally without the necessary approvals or registrations. Buyers may be attracted by exclusive deals or promises of faster transactions without realizing the risks involved. Before proceeding with any property purchase, it is important to verify the broker's credentials and registration through the relevant real estate regulatory authorities. Taking this simple step can help ensure that the transaction is conducted through authorized channels and reduce the risk of avoidable financial and legal complications. Off-Plan Payment Misrepresentation Off-plan properties in the UAE are regulated by clear legal frameworks, but buyers can still face risks when payment terms are misrepresented. This can happen when payment plans are changed unofficially, construction milestones are presented inaccurately, or verbal promises of "guaranteed returns" and fixed completion timelines are used to influence decisions. The key reality for buyers is that returns and delivery schedules are only enforceable if they are clearly stated in the Sale and Purchase Agreement (SPA) and other official documents. Verbal assurances and marketing promises do not carry legal weight on their own. Before committing to an off-plan investment, buyers should carefully review all payment schedules, milestone conditions, and contractual terms and ensure that every promise is documented in writing and supported by the appropriate agreements. False "Guaranteed Rental Returns" Promises Promises of fixed rental returns are another common issue that buyers should approach with caution. Some sellers advertise guaranteed rental yields of 8% to 12% or promise a fixed income for several years to make an investment appear more attractive. In reality, rental performance in the UAE depends on several factors, including market demand, location, property type and condition, and changes in tenant demand and market cycles. Rental yields can fluctuate over time and are influenced by broader market conditions. Buyers should understand that no regulatory authority guarantees rental income from a property investment. Any claims of assured returns should be carefully reviewed and supported by clear contractual terms. Relying solely on marketing promises without proper verification can lead to unrealistic expectations and investment decisions based on assumptions rather than market fundamentals. Fake Title Deeds and Property Ownership Misrepresentation in the UAE Although uncommon, ownership misrepresentation can have serious consequences for buyers. In some cases, buyers may be shown outdated title deeds, properties that are involved in disputes, or units where ownership transfers have not been fully completed. A property is only legally owned when it is officially registered with the relevant land authority, such as the Dubai Land Department in Dubai. Before completing any payment, buyers should verify the property's ownership status and ensure that all documents accurately reflect the current legal position of the asset. Pressure-Based Selling Tactics Some buyers face high-pressure sales tactics, such as claims that a property is the "last available unit," that prices will increase immediately, or that multiple buyers are ready to proceed with the purchase. These tactics can create unnecessary urgency and encourage buyers to skip important verification steps. While market conditions can change, legitimate property transactions in the UAE should allow buyers enough time to review documentation, verify information, and make informed decisions without feeling pressured into committing quickly. Hidden Property Costs and Undisclosed Fees in UAE Real Estate Another common issue in property transactions is incomplete pricing disclosure. Buyers may receive an initial quotation that does not fully account for service charges, transfer fees, registration costs, or ongoing maintenance expenses. As a result, the actual cost of ownership can be significantly higher than expected. Understanding all associated costs in advance is essential for accurate budgeting, return calculations, and long-term investment planning. Duplicate or Re-Sold Units Without Disclosure In some cases, the same property may be listed by multiple agents, shown as available despite being under negotiation, or marketed without updated availability information. This can create confusion for buyers and may lead to booking conflicts or wasted time during the search process. Verifying a property's current status and working with reliable platforms can help reduce the risk of acting on inaccurate availability information. Property Buying Checklist to Avoid Real Estate Scams in the UAE Before making any payment: Verify the broker's licence and registration Confirm the property's ownership status Review the Sale and Purchase Agreement carefully Verify project approvals and payment structure Understand all fees and ownership costs Avoid relying on verbal promises Ensure all commitments are documented in writing How PropertySeller Helps Reduce These Risks At PropertySeller, the focus goes beyond displaying property listings. The platform is designed to reduce decision risk by prioritizing verified property information, clearly structured listing data, and up-to-date availability whenever possible. Duplicate and unconfirmed listings are minimized, and greater emphasis is placed on ownership clarity and legal status. The goal is to provide buyers with transparent information so they can evaluate opportunities with greater confidence and make decisions based on verified details rather than assumptions. Final Takeaway In the UAE property market, the biggest risk is not always outright fraud. More often, problems arise from misinformation, incomplete verification, or misunderstandings about legal processes and ownership. Many buyers do not lose money because of illegal activity. They face difficulties because they rely on marketing claims instead of documentation, overlook important verification steps, or misunderstand the legal structure behind a transaction. A careful approach that prioritizes verification, documentation, and transparency can eliminate many of these risks before they become costly problems. At PropertySeller, the focus is on making the buying process clearer and more reliable by prioritizing verified listings, reducing duplicate and unconfirmed entries, and highlighting ownership status and key property details. The goal is to help buyers make informed decisions based on accurate information and move forward with greater confidence and trust. FAQ’s 1. Are property scams common in the UAE? The UAE property market is highly regulated, but buyers can still face risks from misleading listings, unlicensed intermediaries, incomplete documentation, and misinformation. At PropertySeller, we focus on verified property information and greater transparency to help buyers reduce these risks. 2. How can I verify whether a property listing is genuine? Buyers should verify the property's ownership status, confirm project details, review supporting documents, and work with licensed brokers or trusted platforms. PropertySeller prioritizes verified listings and minimizes duplicate and unconfirmed entries to help buyers make informed decisions. 3. Is it safe to invest in off-plan property in the UAE? Yes, off-plan investments can be safe when projects are properly registered and payments follow regulated procedures. At PropertySeller, we encourage buyers to review all project details, payment schedules, and contractual terms carefully before committing. 4. Who regulates property transactions in Dubai? Property registration and many real estate activities in Dubai are overseen by the Dubai Land Department. Buyers should always ensure transactions are conducted through approved and properly documented channels. 5. How can I check if a real estate broker is licensed? Buyers should verify a broker's registration and credentials through the relevant real estate authorities before proceeding with any transaction. Working with licensed professionals helps reduce the risk of invalid agreements and financial disputes. 6. What should I do before making a property payment? Before making any payment, buyers should confirm ownership status, review all agreements and payment terms, understand the full cost of ownership, and ensure all commitments are documented in writing.

Jun 26, 2026

Read More

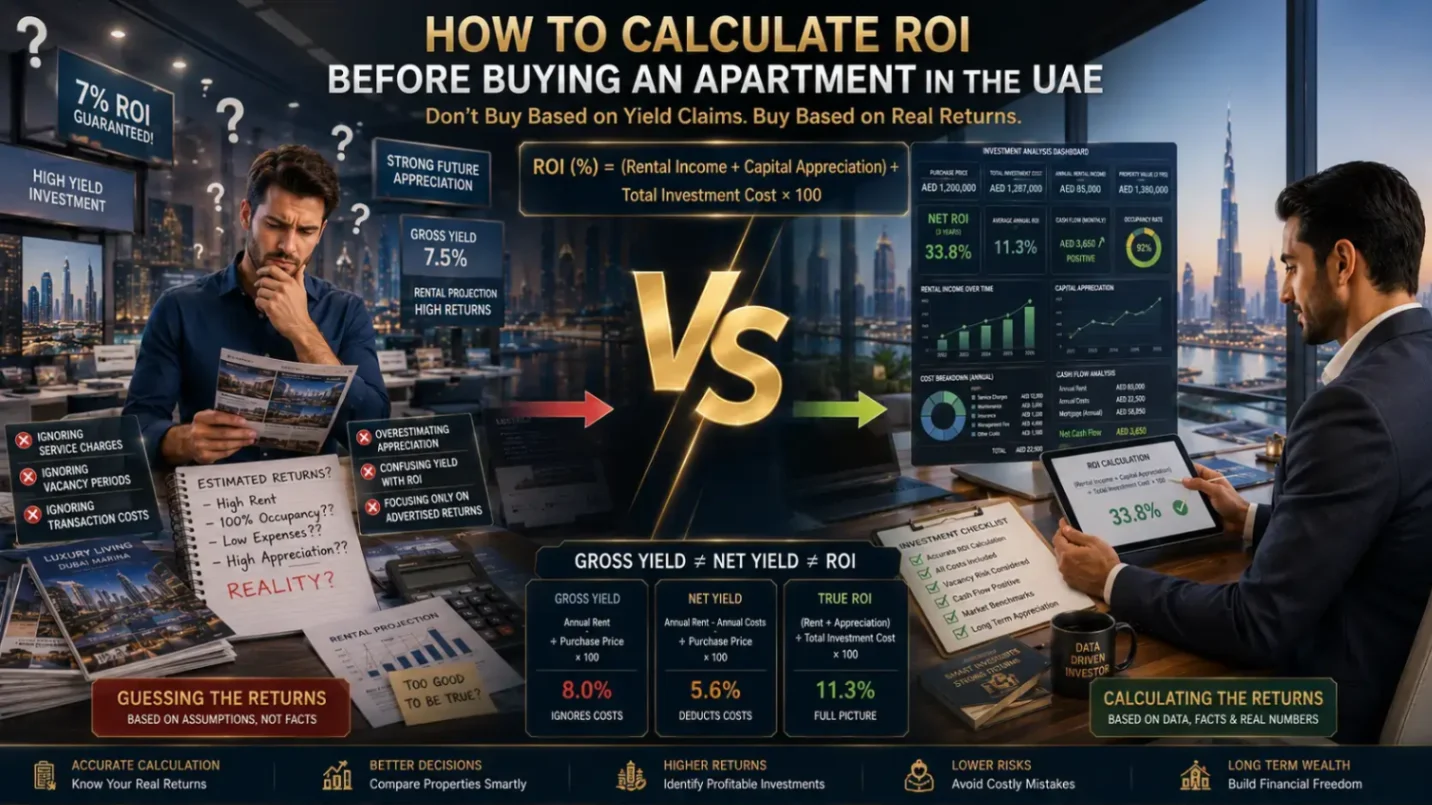

Rental yield is often one of the first figures investors look at when comparing properties in the UAE. A property advertising a 7% or 8% rental yield can seem like an excellent investment. However, many investors make the mistake of focusing only on gross rental income while overlooking one of the biggest ongoing ownership costs: service charges. Service charges can have a significant impact on your actual return on investment (ROI). Two apartments generating the same rental income may produce very different profits simply because one building has substantially higher annual maintenance costs. In this guide, we explain what service charges are, how they are calculated, how they affect your net rental yield and overall ROI, and the key factors investors should consider before buying an apartment in Dubai. What Are Service Charges? Service charges are annual fees paid by apartment owners to cover the maintenance and management of shared areas within a residential building or community. These charges typically contribute towards: Building maintenance Security services Cleaning of common areas Landscaping Swimming pools Gyms Elevator maintenance Building management Shared utilities The exact amount varies depending on the building, location, property size, and the amenities available. While service charges help maintain the quality of a development, they also represent an ongoing cost that directly affects investment returns. Gross Rental Yield vs Net Rental ROI Many property listings advertise gross rental yield. Gross yield is calculated using annual rental income before deducting ownership expenses. However, investors earn net returns, not gross returns. Net Rental ROI considers ongoing costs such as: Service charges Maintenance expenses Property management fees Insurance Vacancy periods Repair costs A property with a slightly lower rental income but lower annual expenses may generate a stronger overall return than one with a higher advertised yield. This is why experienced investors rarely rely on gross rental yield alone. How Service Charges Reduce Rental Returns Every dirham spent on annual service charges reduces your net rental income. For example, imagine two apartments generating similar annual rent. Apartment A has relatively low service charges, while Apartment B is located in a luxury building with premium amenities and significantly higher annual maintenance fees. Although both properties may produce similar rental income, Apartment A could deliver better cash flow because ownership costs are lower. This demonstrates why investors should evaluate both income and expenses before comparing opportunities. Do Higher Service Charges Always Mean a Poor Investment? Not necessarily. Higher service charges often support premium facilities that can increase tenant demand. Luxury developments may offer: Concierge services Fitness centres Swimming pools Children's play areas Landscaped gardens Enhanced security Resident lounges These features can make properties more attractive to tenants and may justify higher rents. The key question isn't whether service charges are high or low. It's whether the additional costs are supported by stronger rental demand, higher occupancy, or improved long-term value. Compare Buildings, Not Just Communities Many investors compare rental yields at the community level, but this approach can overlook important differences between individual buildings. Even within the same neighbourhood, ownership costs can vary significantly from one development to another. Service charges are influenced by factors such as the age of the building, the range of amenities provided, maintenance standards, construction quality, and the effectiveness of the building's management. Properties with extensive facilities or higher operating costs often carry higher annual service charges, which can reduce net rental returns. For this reason, evaluating building-specific ownership costs alongside rental income provides a more accurate picture of an investment's long-term performance than comparing communities alone. How Service Charges Affect Long-Term Cash Flow Rental income generates regular cash flow, but ongoing ownership expenses determine how much of that income is ultimately retained. Service charges are one of the largest recurring costs for apartment owners and should always be factored into investment calculations. Properties with lower annual service charges can contribute to stronger monthly cash flow, improved annual profitability, more predictable investment performance, and higher long-term net returns. Conversely, higher service charges can reduce profitability, particularly during periods of slower rental growth or increased operating costs. By understanding these expenses before purchasing, investors can create more realistic financial projections and compare investment opportunities based on net returns rather than headline rental yields alone. How Service Charges Affect Long-Term Cash Flow Rental income generates regular cash flow, but ongoing ownership expenses determine how much of that income is ultimately retained. Service charges are one of the largest recurring costs for apartment owners and should always be factored into investment calculations. Properties with lower annual service charges can contribute to stronger monthly cash flow, improved annual profitability, more predictable investment performance, and higher long-term net returns. Conversely, higher service charges can reduce profitability, particularly during periods of slower rental growth or increased operating costs. By understanding these expenses before purchasing, investors can create more realistic financial projections and compare investment opportunities based on net returns rather than headline rental yields alone. Balancing Service Charges with Investment Value Service charges are an important part of any investment analysis, but they should not be assessed in isolation. A property with higher annual fees may still deliver stronger overall returns if its location and quality support consistent demand. For example, buildings with strong rental demand, lower vacancy rates, higher tenant retention, premium locations, quality amenities, and solid resale potential can often justify higher service charges through better long-term performance. Likewise, selecting a property solely because it has the lowest service charges may not be the most effective strategy if it compromises rental appeal or future capital growth. The strongest investment decisions come from balancing ongoing ownership costs with a property's long-term income and appreciation potential. Conclusion Service charges are a key part of the total cost of owning an investment property in the UAE and can have a direct impact on your net rental returns. While they reduce annual income, they also help maintain the quality, safety, and long-term appeal of residential buildings and communities. Rather than focusing solely on advertised rental yields, investors should assess the complete financial picture. Comparing service charges alongside rental demand, occupancy levels, maintenance costs, and long-term growth potential provides a more accurate view of a property's investment performance. At PropertySeller, we help investors look beyond headline figures to evaluate the real profitability of a property. By considering both ongoing ownership costs and long-term market fundamentals, buyers can make more informed investment decisions with greater confidence. Frequently Asked Questions 1. How do service charges affect rental ROI in the UAE? Service charges reduce an investor's net rental income, which means they directly influence rental ROI. PropertySeller recommends calculating expected returns after accounting for annual ownership costs rather than relying solely on advertised rental yields. 2. Are higher service charges always bad for property investors? Not necessarily. Higher service charges often support premium amenities that can improve tenant demand and justify higher rental rates. PropertySeller advises investors to assess whether the added costs are matched by stronger rental performance and long-term value. 3. Should I compare service charges before buying an apartment? Yes. Service charges can vary significantly between buildings, even within the same community. PropertySeller helps buyers compare ownership costs alongside rental income and investment potential to make more informed decisions. 4. What costs should I include when calculating rental ROI? In addition to rental income, investors should consider service charges, maintenance, insurance, vacancy periods, property management fees, and financing costs. PropertySeller encourages buyers to focus on net returns rather than gross rental yield. 5. How can I estimate the potential return on an investment property? PropertySeller offers a Rental Income Calculator to estimate rental returns, a Mortgage Calculator to assess financing costs, and an Eligibility Checker to help buyers understand their purchasing power before investing. These tools provide a more complete view of an investment property's financial performance.

Jun 20, 2026

Read More